MG Network

something big isHappening!

In the mean time you can connect with us with via:

- 981-981-9811

- Empire Damansara, Jln PJU 8/8A, Damansara Perdana

- info@moneygrows.net

Copyright ©

Money Grows Network | Theme By Gooyaabi Templates

Money Grows Network

Archive

-

▼

2021

(6029)

-

▼

December

(172)

-

▼

Dec 13

(6)

- Overview of the GBP/USD pair. December 13. The mar...

- Overview of the EUR/USD pair. December 13. The mar...

- Forecast and trading signals for GBP/USD for Decem...

- Forecast and trading signals for EUR/USD on Decemb...

- How to trade GBP/USD on December 13? Simple tips f...

- How to trade EUR/USD on December 13? Simple tips f...

-

▼

Dec 13

(6)

-

▼

December

(172)

- ► 2020 (6116)

- ► 2019 (9411)

- ► 2018 (8656)

- ► 2017 (7162)

- ► 2016 (7614)

- ► 2015 (7602)

Powered by Blogger.

Welcome To Money Grows Network

Tags

Verified By

2006 - 2019 © www.moneygrows.net

Investments in financial products are subject to market risk. Some financial products, such as currency exchange, are highly speculative and any investment should only be done with risk capital. Prices rise and fall and past performance is no assurance of future performance. This website is an information site only.

Popular

-

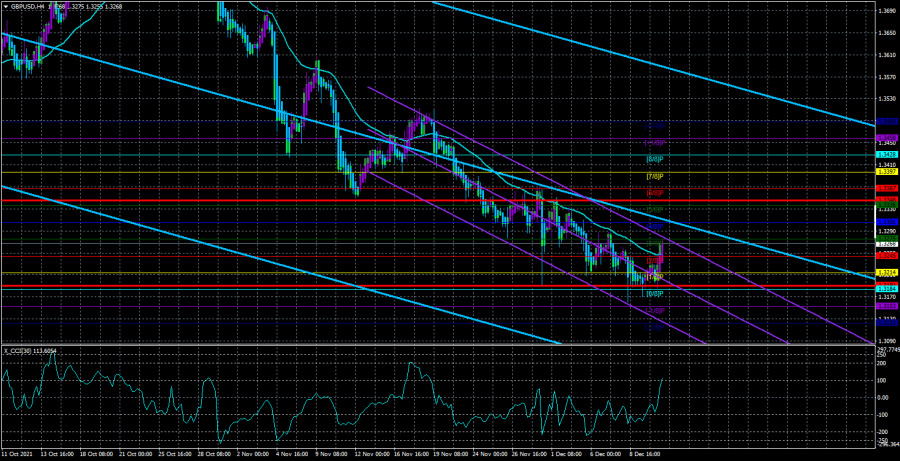

4-hour timeframe Technical details: Higher linear regression channel: direction - downward. Lower linear regression channel: direction -...

-

4-hour timeframe Technical details: Higher linear regression channel: direction - downward. Lower linear regression channel: direction -...

-

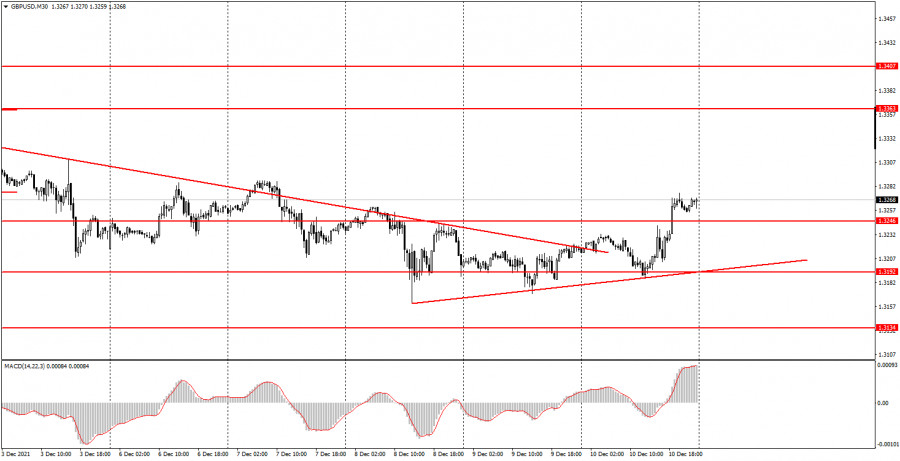

Analysis of previous deals: 30M chart of the GBP/USD pair The GBP/USD pair also resumed a not too strong upward movement on Friday. An up...

-

GBP/USD 5M The GBP/USD pair moved much more "softly" in comparison with the jerky movements of the euro/dollar pair on Friday. T...

-

EUR/USD 5M The EUR/USD pair did not trade in the best way during the last trading day of the week. Of course, the report on inflation in t...

Expert In