The US dollar strengthening due to the de-escalation of the conflict on the Korean Peninsula, the growing probability of the Fed's monetary tightening in December from 36% to 49%, an unpleasant surprise from Chinese demand and growing volumes of shale oil production lowered the prices of futures for Brent and WTI to the three-week lows. The market once again engaged in its favorite activity - a tug of war. Clearly, the reduction in OPEC production increases the possibility of the North Sea oil grade rising to $60 per barrel, but the American hedgers have immediately priced it in. And, contrarily, a drop to $40 per barrel will prompt the cartel to toughen its aggressive commentary, while this will cause shale producers to be worried.

There are so many contradicting information on the market today that even traders with 30-year experience flee from there, claiming that they broke away from the fundamentals and that trading robots have control of the ball. If OPEC begins to hint at extending the agreement beyond March 2018, then this is no longer perceived as a "bullish" signal. This is, rather, a sign of weakness, a forced measure to balance the market. According to the latest IEA study, global reserves at the end of the second quarter declined by 500 000 b/d and amounted to 3 billion b/d. Nevertheless, the figure is higher than the upper ceiling of its five-year average for this period of time, and on the sidelines of the market there are speculations that the cartel requires the extension of the agreement to reduce production for a long period to bring it back to the historical range.

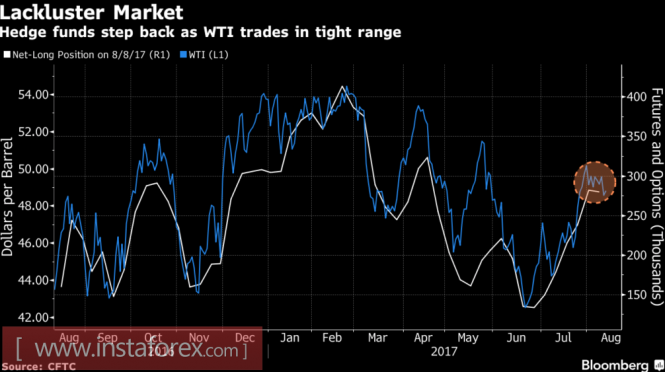

The growing uncertainty makes hedge funds extremely cautious about changing their trading positions. By the end of the week by August 8, net-long positions for WTI increased by a modest 0.8%. This is only the third time this year when the indicator has changed by less than 1%. Speculators are unsure of what to do, and are preferring to wait for new drivers.

The dynamics of oil prices and speculative positions on WTI

Source: Bloomberg.

As soon as information was received that the volume of Chinese oil refining in July fell to the lowest levels since September 2016, while shale oil production forecasts in the US showed the ninth month of gains in September 2017 (6.15 million b/s), these became the basis for closing long positions for Brent and WTI.

Another thing that played a role was the US dollar which strengthened against the backdrop of the moderate "hawkish" comments of New York Fed chief William Dudley. He said he would support the idea of a third hike in the federal funds rate in 2017 if the US economy continues to gain momentum. As a result, the USD index went up, putting pressure on black gold.

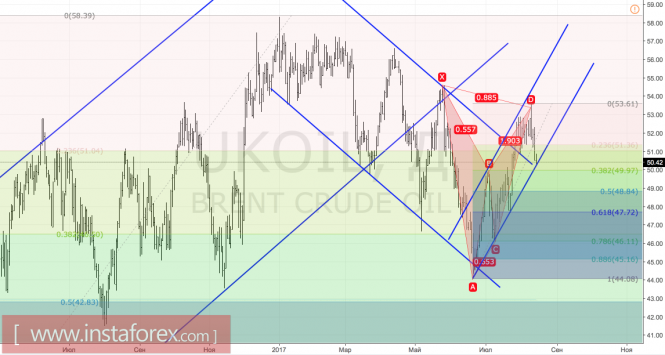

Over the medium term, it is hardly worthwhile to wait for exploits from "bulls" or "bears". The market has found its trading range ($40-60 per barrel) and it is ready to remain in this range for a long time. Technically, it is mirrored in the retreat of Brent quotes to the lower border of the upstream trading channel after the realization of a target of 88.6 percent over the inverted "bat" pattern. The breakthrough of diagonal support will increase the risks of correction in the direction of $48.85 and $47.7. On the contrary, the retreat will bring back the "bulls" to life.

Brent, daily chart