The US dollar, which briskly started the week, lost all of its trump cards and was again sold out on Friday amid muffled data on inflation.

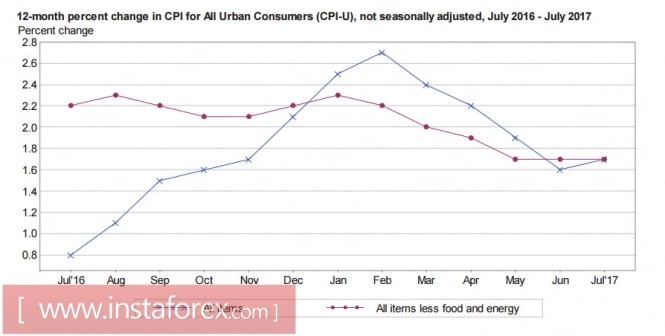

Consumer prices rose by 0.1% in July, an annual increase of 1.7%. Both indicators are better than a month ago, but worse than expected. Experts forecasted prices to rise by 0.2% in the monthly data and 1.8% in the annual data.

Yesterday, the producer prices report was published. It also turned out to be worse than expected. The annual price index rose by 1.9% which is worse than the 2.0% results from the previous month. It is even much worse than the expectation of 2.2%. Compared to the results from June, prices have dropped by 0.1%. The worse-than-expected data indicates that there is still a significant imbalance in the market between estimates of the state of the US economy and real macroeconomic indicators.

The head of the Federal Reserve Bank of Minneapolis, Neel Kashkari, said on Friday that the US Federal Reserve can wait in increasing interest rates until inflation approaches the target of 2%. Kashkari drew attention the fact that the wage growth remains slow and a premature rate increase may lead to a slowdown in economic growth.

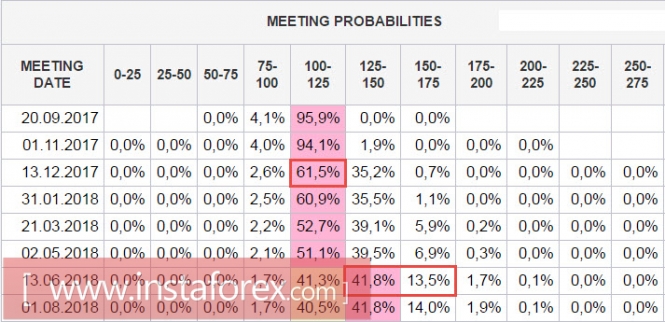

In fact, over the past week, the probability of a rate hike in December, according to the CME, fell from 48% to 35.9%. The expectations of this next step by the Fed moved to June 2018. The shift of expectations for six months is a lot. In fact, bulls in dollars are deprived reasons to go on the offensive in the foreseeable future.

Another factor of the weakness of the dollar was the geopolitical tensions on the Korean peninsula. US President Donald Trump warned Pyongyang against attacks on Guam, where the US military base is located or on US allies. The markets began to respond to the verbal war, but the probability of a military solution to the issue at the moment is extremely small. The probability of a strike against North Korea will cause Russia to be extremely displeased with China and will promote an even closer rapprochement which clearly does not meet the long-term interests of the United States.

A noticeable increase in the degree of tension is not accidental and quite possibly intended to hide something more substantial than Pyongyang's nuclear program. On Thursday, the Treasury report on the budget was published despite the annual dynamics for 17 months. Revenue growth cannot compensate for the decline of the previous period and ensure the fulfillment of government obligations. Perhaps Trump's formidable rhetoric about North Korea is of an intra-American nature. Trump tries to score points before a large-scale battle with the Congress on a number of crucial issues. Hour X is approaching, the government must submit a draft budget for the 2018 financial year. In any case, it is impossible to balance falling incomes with expenditures without raising the ceiling of borrowing. Moreover, the formation of budget is meaningless without the approval of a tax reform, the project of which has not yet been submitted to the Congress. Perhaps Trump's administration will try to combine these two issues into one. The markets expect active government action in the near future.

On Tuesday, data on retail sales and import and export prices will be published in July. Forecasts are moderately positive. If the released data is no worse than expectations, it can stop the decline in the dollar. On Wednesday, the market's attention will be focused on the publication of the protocol of the July FOMC meeting. Players will assess the likelihood of the start of a quantitative tightening program in September.

In any case, there are more questions than answers. The dollar cannot rely on either economic growth or geopolitical stability. While there is advantage over defensive assets, primarily for yen and gold, there is a high probability that this mood will continue for the upcoming week.

The material has been provided by InstaForex Company - www.instaforex.com