Eurozone

Today, the ECB will hold a regular meeting on monetary policy. Investors are waiting for clarity on the further plans of the regulator. Particularly, the decision of Mario Draghi whether to give more or less clear guidance regarding the curtailment timing of the asset repurchase program, and whether the issue of a strong euro will be raised at the meeting.

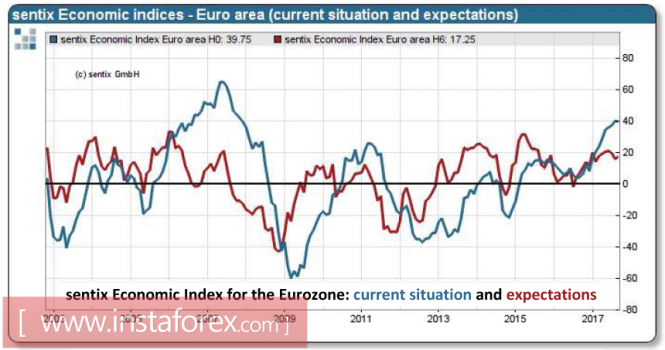

Since January, the EURUSD rate has increased by more than 15%, and further growth caused an increasing concern among exporters, and also acts as a deterrent to the growth of inflation. While the economic state of the euro area still has no cause for concern. Business activity is at the multi-year highs, as the Sentix index for the euro area reached 28.2p. The current state estimate rose to 39.75p, which is the best result since 2008.

The index notably improved its position in the US, which further reflects global growth. With a number of key parameters, the euro economy looks much more confident. The growth of the euro seems in good condition upon assessing the investors' prospects, together with the urgent need to abolish the incentive program.

On the opening of the ECB meeting which talks about the regulator's concern about high rate and the intention to consider the issue of increasing incentives in October or even December has somewhat cooled the ardor of bulls, however, there is no doubt for a reversal. Even if Draghi is able to evade any and will not give the bulls a single driver, even in this case the euro will look stronger and a reversal might occur only against the background of simultaneously relevant news from the US.

Yesterday, reports say that President Trump managed to agree with the Congress on postponing the decision of the state regarding the debt issue until December 15. This news was received positively by the market but its significance is not high because the Republicans did not support Trump generally, which shows the depth of the split in power circles

Disposition of the euro is as follows.United Kingdom

The pound continues to hold in the ascending channel.

Brexit negotiations still don't have any progress made, and in fact, the pound does not have many positive factors that can support its growth. Nevertheless, while the US receives mainly bearish signals, it is not necessary to wait for the pivot to turn southwards. The growth in the 1.3130 / 40 region is still possible, depending on the external situation, either correction or sideways range, an exit will follow.

Oil and ruble

US Crude oil reserves increased by 2.79 million barrels last week, according to the API. But the market ignored this clearly bearish factor. Brent climbed above $ 54/bbl while the WTI reach $ 49/bbl. As of this writing, the main driver is the recovery in production in Texas and the related increase in demand for oil. Moreover, as hurricane Irma approaches to the shores of Florida, it supports the demand for gasoline, hence, the decline in oil prices in the following days is improbable.

The growth of oil prices provide support to the Russian ruble, but in the current coordinates, this driver is far from the main one. The Department of Research and Forecasting of the Bank of Russia raised the forecast for GDP growth rates in 2017, from 1.5% to 2.0%. This is because of the combined drop in inflation to a historically low level of 3.3% and the outpacing real wage growth, which indicates the sustainability of the Russian economy that will lead to an increase in demand for ruble denominated assets. Expectations about the ability of the CBR to a more aggressive rate cut increase. The markets are waiting for an increase in capital inflows.

For the ruble, the conditions are more than favorable, as it moves towards the level of 56.1 rubles/dollar. It is still more likely to take the sideways range or correction.

The material has been provided by InstaForex Company - www.instaforex.com