On Friday, the US Congress passed a law on the temporary increase of the US public debt ceiling until December 8 and on the provision of $15.25 billion to remove the consequences of Hurricane Harvey. The decision, which was made possible by Trump's approval and the leadership of the Democratic Party, was not given to Congress easily, because the agreement was too short, adopted in an emergency, and moreover, Trump's government succeeded in removing the promise to cut government spending from the final wording.

Meanwhile, the situation with budget revenues continues to deteriorate. The US Committee on the Budget of the Congress published another update, which noted that in the 11 months of the 2017 financial year, the deficit amounted to 675 billion dollars, which is 56 billion higher than last year, and a negative trend persists. Despite the fact that budget revenues are higher than a year ago, expenditures increase at a much higher rate, and the absence of a plan to cut spending in the state debt law will contribute to the growth of the budget deficit.

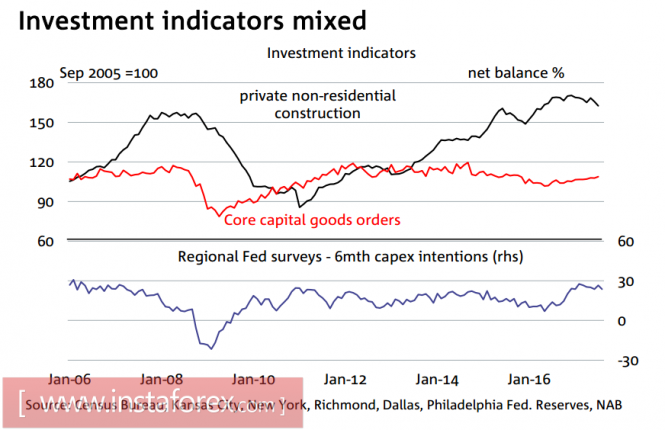

The pace of business lending growth remains low. The positive momentum from the mining sector is beginning to slow down, the cost of building non-residential premises shows negative dynamics, the growth rates of sales of residential premises are also slowing down. Regional business activity indices after a period of growth in the second half of 2016 also show a clear downward trend.

The president of the Federal Reserve Bank of New York, William Dudley, said on Friday that he expects further interest rate increases, but he does not know exactly when the next raise will be. Dudley's speech was expected by the market with increased attention, since after the clearly dovish speeches of several cabinet members at the beginning of the week and the news about the voluntary resignation from the post of Deputy Chairman of the Federal Reserve Stanley Fisher, investors were waiting for at least some positive information. Dudley, however, preferred vague comments, saying that the increase in rates will depend on how the situation in the economy will develop. Dudley also said that inflation is well below the target level of 2%, so soft financial conditions should not cause concern.

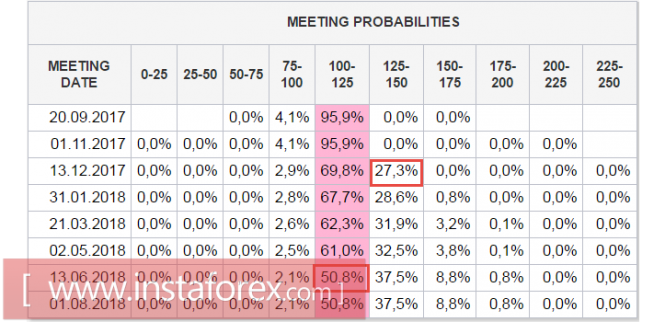

Investors are prepared to the face the fact that the Fed will not be able to implement its plan to normalize monetary policy, given that there are no conditions for another rate increase this year. Moreover, for the first time since June 2016, the probability of a rate increase, according to CME, is below 50%. This result indicates the complete disappointment of investors in the current economic course.

The next extended meeting of the FOMC is in 10 days. Markets are almost certain that the Fed will announce the beginning of a phased reduction of the balance sheet, but the strategy of justifying such a step will be of most interest. The reduction of the balance means not only reducing assets on the account of the Fed, but also a cut in liabilities. To date, the balance sheet structure contains 4.53 trillion Federal Reserve securities, of which 1.57 trillion is the currency in circulation, and 2.37 trillion are surplus reserves of commercial banks on the Fed's correspondent accounts. Obviously, the reduction in the balance sheet should be accompanied by the repayment of obligations, and therefore investors fairly expect changes in the policy of charging interest on excess reserves.

In other words, commercial banks should start withdrawing their funds from the accounts of the Fed because of a decline in yield. In order for this process to be regulated, new tools for investing in the United States are needed. If inflation continues to decline, the spread of yields between US securities and, for example, Europe, will also tend to decline, which further refocuses capital flows in favor of European assets.

Thus, for the dollar, the situation continues to be negative. Investors do not expect it to turn positive and do not see any reason to change their view: the dollar outflow will continue. On Monday, the tendency toward a decline in the dollar can undergo development against the background of the absence of any positive macroeconomic factors.

The material has been provided by InstaForex Company - www.instaforex.com