Eurozone

The indicator of economic sentiment ZEW in Germany rose to 17.6 points in October. The growth is not as strong compared in the previous months but it still reflects positive changes in the economy. In the euro area as a whole, the index fell from 31.7 to 26.7 points but is still in the zone of two-year highs.

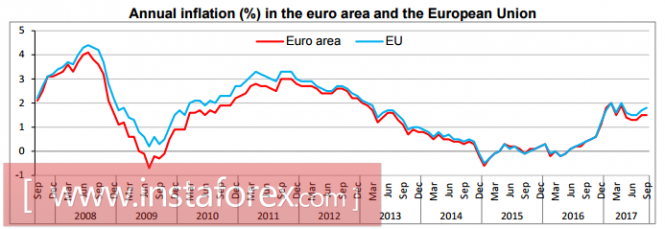

The inflation in September increased by 0.4%, which is higher than + 0.3% in August while the year-on-year growth was 1.5% higher than the month earlier. The root value excluding food and energy resources in contrary to forecasts was kept at 1.3%, which can be regarded as a positive for the euro currency.

The intensity of the confrontation regarding the prospects for the curtailment of the asset repurchase program is not decreasing. The Constitutional Court of Germany on Wednesday rejected another request of the Bundesbank on the right to cease participation in the asset repurchase program. Even if considering this process, the ECB will be seriously limited in its capabilities. Mario Draghi in his next speech denied the thesis that the ECB's buyout program prevents structural reforms in the euro area countries. In his opinion, low rates promote reforms as they create favorable macroeconomic conditions.

The ECB obviously resists the growth of the euro. While one of the formal main criteria is inflation and being below the target, these do not intend to make changes to the monetary policy. These expectations put pressure on the euro before the ECB meeting on October 26, whereas the attention this time will be higher than usual.

The euro lost its driver to growth and it is behind the momentum of the dollar. The decrease to support area of 1.1660 / 75 with the subsequent move to 1.1550 is highly probable.

United Kingdom

The pound received support on Tuesday after the publication of data on consumer inflation, which in September rose to 3.0% year on year from 2.9% a month earlier. At the same time, a number of other price indicators, such as producer prices or the retail price index, demonstrate a slowdown in growth rates. Generally, this led the market to believe that price growth is not so convincing as to predict a confident increase in the rate by the Bank of England at its meeting on November 2.

A day later, the employment report came out. The Unemployment was expected to remain at 4.3% in August, which is close to full employment. On the other hand, the average salary growth was slightly better than expected at 2.1%, but it was slightly worse than 2.2% of the previous month. These data cannot be considered a bullish factor for the pound. At least this could because of a simple reason, the wage growth lags behind inflation and is substantially lower than two years ago. In fact, the labor market does not support price increases. Therefore, high inflation is a consequence of rising import prices after the fall of the pound a year ago, and not a reflection of growing consumer demand.

imports coming from the EU will become even more expensive if a mutually acceptable solution is not found. This will be a factor in favor of inflation but not in the economic growth because this can provoke an increase in the lending of households against the backdrop of weak income growth. Eventually, this will eventually hit consumer activity.

The pound continues to trade in the wide range of 1.3350 / 3050, the probability of moving towards the lows of the month is increasing.

The material has been provided by InstaForex Company - www.instaforex.com