Eurozone

The first signs of a decline in activity in the eurozone increase the chances of a reversal in the main currency pair in favor of the dollar.

The confidence index of Sentix investors decreased in December to 31.1 points, which is lower than the forecast of 33.6 points and lower than the level of November reading of 34 points. Activity is still at a record high, but there are not enough objective factors to support growth. PMI indexes from Markit for November in the sector of services and manufacturing were respectively 56.2p and 57.5p, which corresponded to the forecasts and the result of October. Activity, therefore, is still high, but growth has stopped.

Producer price growth slowed to 2.5% in October against 2.8% a month earlier, retail sales in November decreased by 1.1%, and annual growth was only 0.4%, which is clearly not enough to rely on consumer spending growth and as a consequence - increase in inflation.

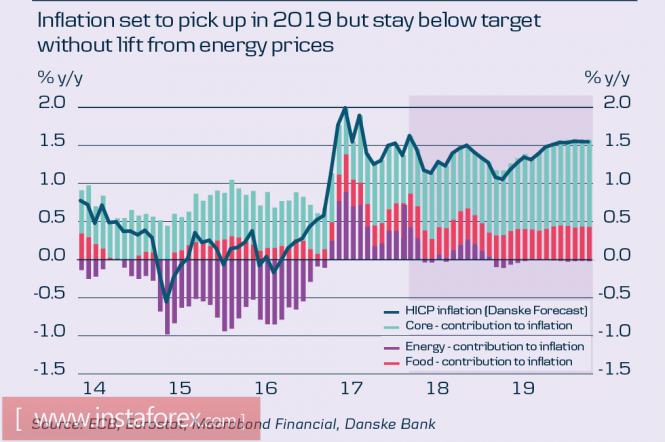

Inflation remains below the target, but the ECB believes that inflation will continue to grow, but many observers note that there are few objective prerequisites for the growth of consumer prices. Danske Bank believes that the core inflation in 2018 will not exceed 1.1% and this point of view is shared by many.

On December 14, the ECB meeting on monetary policy will take place. Until recently, the mood was quite optimistic, with players expecting the ECB will announce a more aggressive exit from soft monetary policy. However, a deterioration in the overall picture with consumer demand increases the likelihood of more cautious forecasts. Upping the rate in the next year's perspective is not expected, which automatically indicates an increase in the yield spread in favor of the dollar.

The probability of returning EURUSD to 1.20 looks idealistic at the current moment. A more reasonable scenario is the decline to the November low at 1.1550, followed by its update and a move to 1.14 over the medium term. The dynamics of the euro will depend on the publication on Friday of the report on employment in the US, expectations on which are optimistic and do not contribute to the return of bullish sentiment on the euro.

United Kingdom

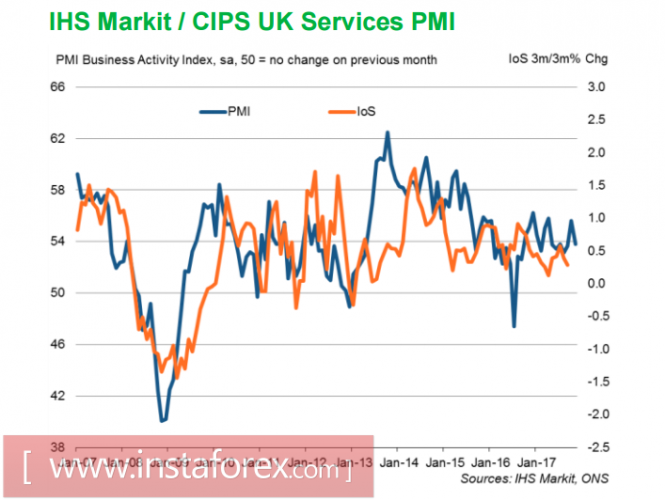

Business activity in the services sector of the UK declined in November to 53.8p against 55.6p a month earlier, and this is well below the forecasts of 55.0p.

Economic growth in the country is slowing, and the UK is among the group with the weakest GDP growth among EC28. The reason was voiced repeatedly - high inflation combined with low growth rates of average wages lead to a decrease in consumption, which is the main engine of economic growth. Exit from this situation is not visible in the short term, and therefore the forecast for GDP growth rates remains unfavorable. The Bank of England sees it at 1.5% in 2018, which is clearly not enough for sustainable development.

The development of the Brexit situation is far from ideal, much will depend on whether it will be possible to reach a consensus on the first phase of negotiations before the EU summit on December 14.

The Bank of England is unlikely to raise interest rates further in the foreseeable future, which worsens the pound's position relative to the US dollar. The highs set in September at 1.3656 is highly unlikely to be updated in the medium term, the pound will seek a strong support line of 1.30, and most likely it will not stand.

Oil

Oil dropped significantly on Wednesday, Brent lost 2.5%, losing the driver for growth. The first sign of the approaching correction was the report of the US Energy Ministry, which reported an increase in production of 9.707 million barrels per day, as well as the record reserves of gasoline, which indicates a reduction in demand.

The decline did not lead to panic, as the correction after the OPEC+ meeting was expected, and now oil will spend some time in the lateral range until new drivers are developed.

The material has been provided by InstaForex Company - www.instaforex.com