Eurozone

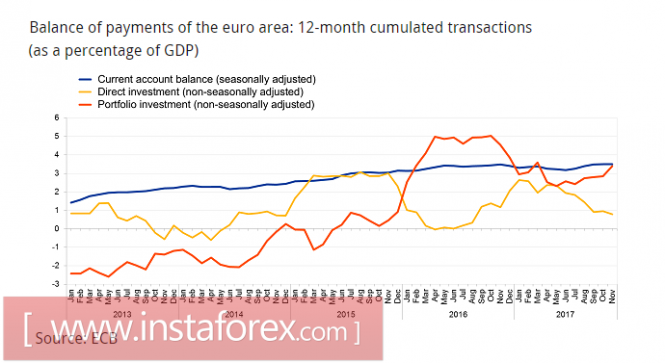

While the United States is shaking with political storms, the eurozone is confidently moving towards economic prosperity. In any case, such a conclusion is quite appropriate against the background of improving the majority of macroeconomic indicators. The balance of the current account reached a trade surplus of 32.5 billion euros in November, along with an increase in all indicators, except for secondary income.

The eurozone and especially Germany have traditionally been criticized for too much trade surplus. The head of the IMF, Lagarde, said on Friday that the IMF was worried about the current situation, and a decrease in Germany's surplus would reduce global disparities. Lagarde calls for lowering the surplus by increasing imports and domestic spending, which is equivalent to the proposal to contribute to the growth of the euro.

The head of the Bundesbank Weidmann is strongly opposed to this approach, because, in his opinion, the aging of the German population will lead to an increase in domestic spending, and therefore one should not try to "help the neighbors" in this way.

On January 25, the ECB will hold a regular meeting on monetary policy, the markets do not expect any changes, and announcement of the date for the completion of the asset repurchase program is expected not earlier than March, as in January there will be no publication of updated macroeconomic forecasts. At the same time, a more aggressive tone of Mario Draghi's comments is possible, which is interested in somewhat limiting the demand for the euro.

On Tuesday, ZEW's report on moods in the business area of the eurozone will be published, the outlook is positive, and the euro can get support. On Wednesday - the forecast for PMI Markit indices is also positive. On Monday, the euro could take a pause to form a new driver for growth, quotes will remain, most likely, in the trading range of 1.2092/1.2323.

There may be disruption in plans from unexpected results of voting in Germany by the SPD this Sunday on the agreement on the government coalition. In case of a negative outcome of the vote, the euro may open with a gap in trading on Monday and go below 1.20.

United Kingdom

Despite confidently positive forecasts, instead of the expected growth, retail sales in December for 2017 showed a decline in volumes, with the cumulative growth only 1.4%. In December there was a decrease of 1.5% compared to November, despite the usual growth for this month due to Christmas sales.

Retail data show that the increase in consumer inflation, which is declared to be the reason for the Bank of England to raise the rate, does not really have any solid ground and is caused solely by the appreciation of imports due to the fall of the pound after Brexit. The Bank of England, thus, raised the rate not to curb inflation, but to create a positive background in the struggle for financial flows between London and Brussels.

On Wednesday, a report on the labor market will be published and according to majority of estimates, there are signs that employment is no longer growing at the same rate and will remain at 4.3% or even fall to 4.4%. As for the growth of average wages, the forecast is a decline to 2.2%, which may lead to selling of the pound if the forecasts are confirmed.

On Friday, the first preliminary estimate of GDP in the fourth quarter is expected. According to PMI, the growth should be in the range of 0.4% -0.5%, but NIESR recently forecasted a 0.6% growth, and therefore the data can exceed the market's expectations.

The pound has made notable progress, recovering all losses after Brexit, the momentum is still strong, and if it is supported by a report on the labor market, the pound will be able to gain a foothold above 1.40. Growth is supported by the demand for risk and the fundamental weakness of the dollar, which is increasingly difficult to conceal.

Oil

Oil somewhat slowed down its rally and the correction on Brent allowed the quotes to drop below $ 68/bpd, but there are still no reasons for a deeper decline. Corrective sentiment can prevail if markets do not find an additional driver for growth, until such is found and trade goes to the lateral range.

IEA predicts a sharp increase in the production of shale oil in the US due to rising prices, but there is no evidence of increased investment in the industry. With regards to Russia, the IEA notes a noticeable increase in revenues, even as output declines.

While market participants are looking for a new driver, the oil goes into the lateral range, but the resumption of attempts to update the highs at this stage looks a little more likely.

The material has been provided by InstaForex Company - www.instaforex.com