Eurozone

Markets continue to assess under the microscope the results of the ECB meeting on Thursday. Mario Draghi's press conference started with a few dovish statements, as Draghi focused on the slowness and austerity, indicating that it is not necessary to wait for surprises and, especially, some severe steps from the ECB.

Draghi called for dividing the expectations for the rate and the regulation of the asset purchase program. Regarding the rate, Draghi spoke directly, he said, the chances of an increase this year are small. With regards to the repurchase of assets, the position is more hawkish, as Draghi had to declare sustainable economic growth, which could mean confirmation of plans to curtail the repurchase program.

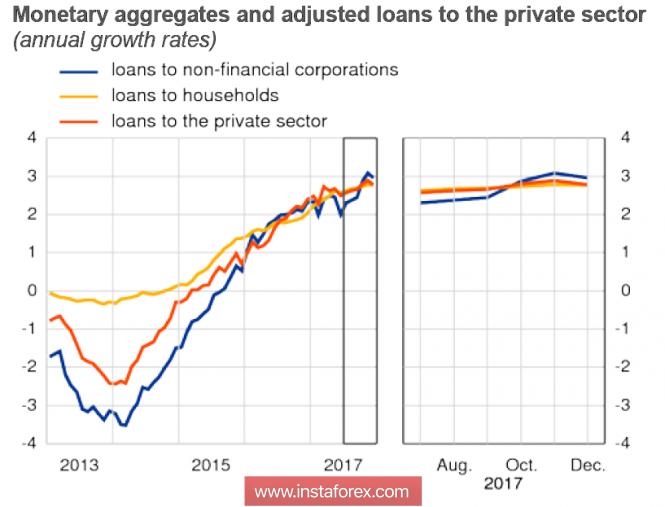

The ECB's lending report released on Friday showed that in December the growth rate of lending to the private sector and non-financial organizations slowed somewhat, but annual rates remain firmly strong, which confirms the conclusion about the sustainability of economic growth in the euro area.

A member of the ECB Executive Board, Benoit Coeure, commented on US Treasury Secretary Munchin's previous statements, saying that attempts to target exchange rates could provoke a currency war, and this is the last thing the world needs. On Thursday, indicating a similar tone, Draghi spoke out, as the issue for the euro is important - excessive strengthening can put downward pressure on inflation, as imports cheapen.

On Tuesday, a preliminary GDP report will be released for the fourth quarter, with a forecast of a 2.6% growth, which is no worse than in the US, which means it will support the euro, all other things being equal. On Wednesday, the report on inflation in January will be released, the forecast is negative, the euro could be under pressure. In general, the reasons for the euro to continue growth without a correction are few, likely a decrease to 1.2323 and consolidation just below the peaks that were reached.

United Kingdom

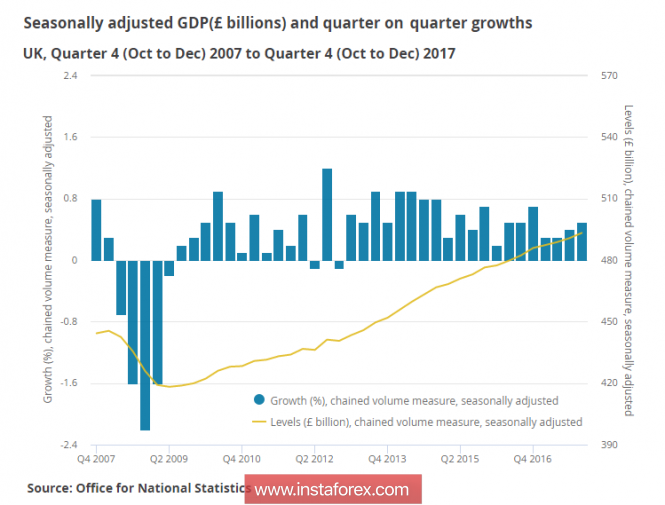

The UK economy grew slightly stronger in the fourth quarter than forecast, which had a limited support for the pound, which once again renewed its peak after Brexit. However, NIESR forecasted the possibility of growth up to 0.6%, so the market was not very surprised by the result.

The head of the Bank of England, Mark Carney, made an attempt on Friday to knock down a wave of demand for the pound, which, however, proved unsuccessful. Answering a question in an interview with the BBC about quantifying damage from Brexit, Carney said that the country's GDP lost 1% of its growth rate, and by the end of 2018 these losses will grow to 2%. To date, the result of Brexit has been a decline in economic activity of tens of billions of pounds, and it takes time to achieve a higher growth potential.

Carney highlighted the main point - companies are cutting back on investments, as they are waiting for clarity on the UK's trading positions after it leaves the EU.

On Tuesday, the Bank of England will report on consumer and mortgage lending in December. On Wednesday, the Gfk index on consumer confidence will be released. The pound looked very strong last week, and went far into the overbought zone, but the momentum is still strong, and therefore the highs will likely be updated, the nearest support is 1.3995.

Oil

Oil adheres to the most likely scenario, once again the peak is updated, the trends remain the same. Saudi Energy Minister Khaled al-Faleh said in Davos that $25 from its current price is secured by the OPEC + deal, confirming the cartel's position to adhere to the plan to stabilize the market. There is no reason to expect that the OPEC + countries will voluntarily give up the mechanism that fills the scarce state budgets of the oil-producing countries.The material has been provided by InstaForex Company - www.instaforex.com