The US dollar ended the week with a decline once more after failing to find a driver to return to the path of growth. The decline happens against the background of improved macroeconomic parameters within the US, which somewhat discourages the bulls. who cannot regain the initiative in any way.

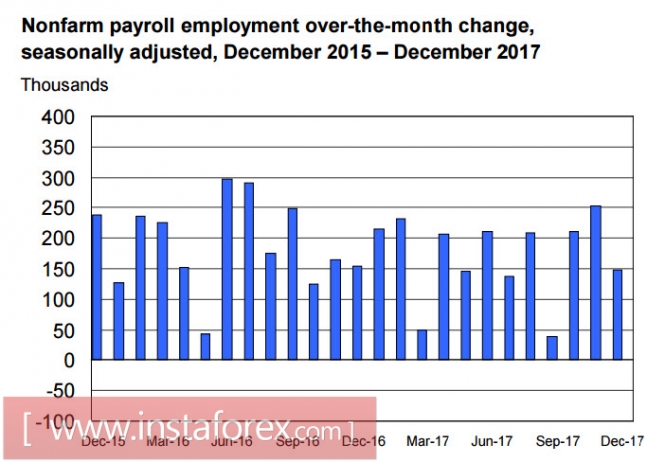

The December employment report, published on Friday, was worse than forecast. The number of new jobs in the non-agricultural sector increased by 148 thousand with a forecast of 190 thousand. The unemployment rate remained unchanged for the third consecutive month and is at 4.1%. The average hourly wage rose by 2.5% which is slightly higher than 2.4% a month earlier.

In total for 2017, 2.06 million new jobs were created. This is less than in 2016 but significantly more than forecasted. In order to ensure that unemployment does not exceed the current levels, it is enough to create 100 thousand jobs a month. This means that the labor market as a whole continues to grow

The dollar looks weak in recent weeks as investors' appetite for risk is growing amid positive expectations for the global economy. Significantly stronger data than forecasted from China is supported by a global trend towards an increase in activity and contributes to a rise in raw material prices while business activity growth also leads to an increase in demand for the dollar. These are actively used to increase lending to projects in local currencies.

The dollar may remain under pressure for a fairly long time or at least as long as the investment recovery continues in emerging markets and in the commodity sector. The capital does not see the need to remain inside the US, even despite the adoption of the law on tax reform. It diverges around the world in search of higher returns.

There are growing concerns about the Fed's ability to raise rates. Despite the fact that the official explanation for the need to raise rates is to contain inflation, current levels of consumer activity are not high enough to take this argument seriously. Inflation remains below the 2% target and the new tax reform will contribute to the growth of the budget deficit. So, raising rates will lead to an increase in the cost of debt servicing at all levels amid unconvincing economic growth. This may ultimately lead to a recession rather than growth.

The dynamics of yields of inflation-protected 5-year bonds shows that investors as a whole are inclined to believe that inflation will resume its growth. This confidence is in favor of the Fed and may ultimately support the dollar.

Next week will be quite saturated with macroeconomic publications. Business life will enter the usual rhythm. On Monday, the Fed will report on the dynamics of consumer loans in November. The publication is important in terms of assessing the activity of consumers and forecasting about the growth of inflation. On Tuesday, NFIB will submit a report on the level of confidence in small businesses for the month of December. For more than a year, this indicator has been at record high levels, supporting positive economic expectations.

On Wednesday, the US Department of Labor will publish a report on the dynamics of prices for imports and exports. On Thursday, a report will be released on producer price indices while on Friday the main report of the week will be released - the data on consumer inflation and retail sales. The main focus will be on the inflation core which reflects consumer demand without taking into account food and energy prices. While the forecast of experts is optimistic, it is expected to grow to 1.8% against 1.7% in November. The release of the data will support the dollar no worse than expectations.

Also next week, several members of the FOMC are expected to speak, which may change expectations for the next rate increase at the March meeting. At the current stage, all attention will be directed to the first results of the tax reform, which can adjust the Fed's plans for the rate.

The dollar positions look neutral at this stage. Against commodity currencies, it will remain under pressure but against the yen and the European currencies, the decline may come to an end in the near future.

The material has been provided by InstaForex Company - www.instaforex.com