Eurozone

Economic prospects for the euro area remain stable, statistics in favor of the euro. Germany, as the locomotive of the entire eurozone, continues to please investors with the growth of all key indicators. The industrial production in November increased by 3.4%, year-on-year growth was already 5.6%, this is the best result for 6 years. The trade balance is confidently surplus, the budget deficit is eliminated, the ratio of the national debt to GDP is steadily declining.

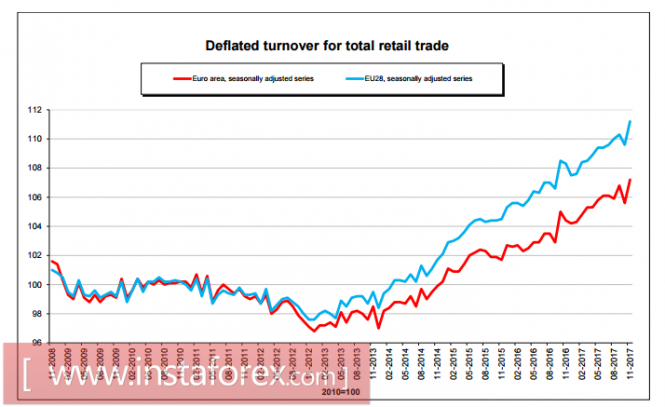

The economy of the euro area as a whole is also on the rise. According to the European Commission, the index of business sentiment is at record levels for the entire history of observations, a similar result is the confidence index from Sentix, which rose in January to 32.9p, exceeding forecasts. The growth of retail sales in November has sharply accelerated, which gives grounds to count on the growth of consumer activity.

In general, the economic situation supports the euro more strongly than one would have guessed if we focus on the dynamics of spreads. The yields of 10-year US bonds are steadily growing, as the Fed continues tightening policy, but investors are not in a hurry to withdraw their capital to the US due to unclear economic prospects.

The euro continues to hold positions near the reached highs, the further movement will depend on the publication of data on inflation in the USA on Friday. At the moment, EUR/USD forms the second peak near the resistance 1.20, following the results of the week the rate may decrease to 1.1880. However, it is too early to speak about changing the orientation to the south.

The United Kingdom

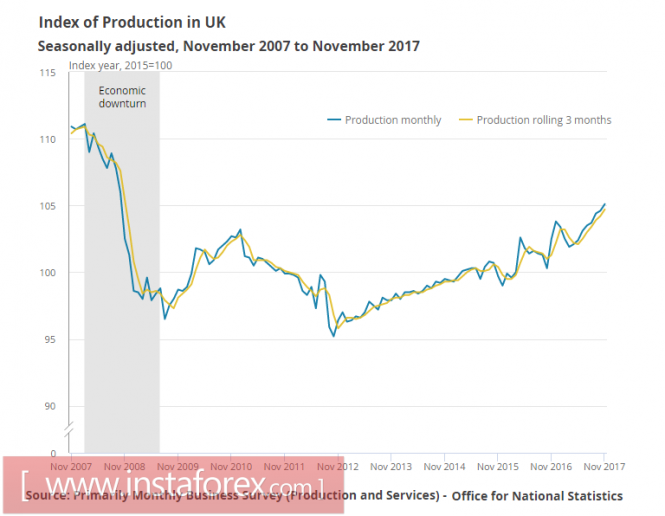

The pound received several positive signals this week, which allowed it to stay on the growth trajectory against the dollar. Retail sales, according to BRC, rose 0.6% in December, exceeding the forecast of 0.4% and positively affecting consumer activity, which is still too low. The growth of industrial production in November significantly exceeded forecasts, that is, the expected decline was not deep.

NIESR published an estimate of GDP growth for the last three months to December inclusive, it was 0.6%, which is higher than the forecast of 0.5% and, especially, above the previous estimate in November of 0.4%. In total, NIESR expects to see growth in 2017, 1.8%, slightly higher than the preliminary estimates voiced earlier.

Usually, NIESR forecasts cause interest before the quarterly meetings of the Bank of England, as they allow to assess possible changes in macroeconomic forecasts. However, until the next BoE meeting on February 8 is still quite a lot of time, so the pound calmly reacted to good reporting. Pound movements until the end of the week will depend on external factors, which will give additional chances to the bears. The pound is under pressure, most likely the decline to support 1.3420.

Oil and the ruble

The commodity stocks of oil in the US, according to the Ministry of Energy, fell by 4.9 million barrels last week, which led to an increase in oil quotations. Traders did not react to the deceleration of production at once by 290 thousand barrels per day, or on the tension around Iran, which may end with another attempt of sanctions pressure from the US. Winter is approaching the equator, which means that the end of the seasonal demand factor is approaching.

All these factors under other circumstances could provoke a corrective decline, but the market is still focused on the general interest of growth to risk, supported by high rates of global recovery. The oil is moving to new highs. If nothing unexpected happens, the market will see Brent reaching the level of $ 70 / bbl. already in the next few days.

The ruble reacts weakly to rising oil prices, awaiting news from the Ministry of Finance about the possible introduction of new rules for buying foreign currency. The gradual withdrawal from the speculative capital market, caused by the planned reduction in the CBR's rate, is affecting, however, the influx of portfolio investments is growing. The ruble has no direction and can stay at current levels until the end of the week.

The material has been provided by InstaForex Company - www.instaforex.com