Eurozone

The euro has been under pressure since the beginning of the week, because even the background of weak dollar published macroeconomic data looked unexpectedly weak.

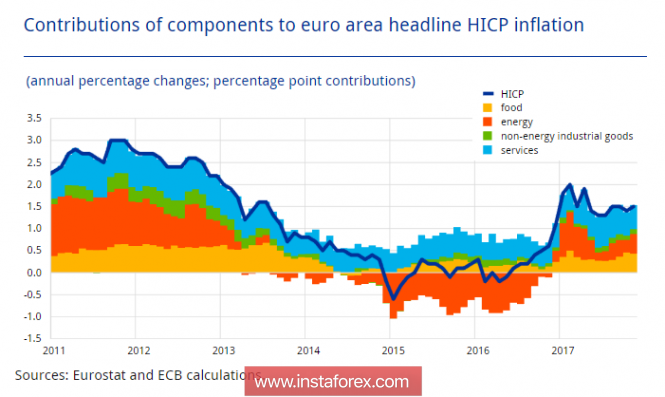

The preliminary data on eurozone GDP in the fourth quarter reached 2.6%, slightly lower than the forecast of 2.7%. The entire package of economic activity indexes in January from the European Commission was unexpectedly in the red zone, although experts predicted a steady growth. Also, with a drop in data on consumer inflation in Germany, the negative area also left data on retail sales in December, that is, even traditional Christmas sales did not have any positive effect.

Accordingly, inflation data in the eurozone as a whole also turned out to be worse than in December. A decline to 1.3% against 1.4% and to 1.0% without taking into account energy and food prices. The stabilization of inflation in the second half of the year is now under threat.

The euro reacted with the decrease, as any negative gives the ECB a delay with the completion of the incentive program. At the same time, long-term criteria are still in favor of the euro, the policy of weakening the dollar, taken by the Trump administration, will remain the dominant factor in the long run.

The movement before the publication of the employment report will be predominantly in the lateral range, the main support is 1.2323, while the pair above, the trend will remain ascending.

The United Kingdom

Unlike the euro area, the pound news was more positive.

The volume of consumer lending grew significantly in December, according to the Bank of England, while at the same time the number of approved applications for mortgages decreased. The latter parameter reflects the general slowdown in construction in the country before the threat of rising interest rates.

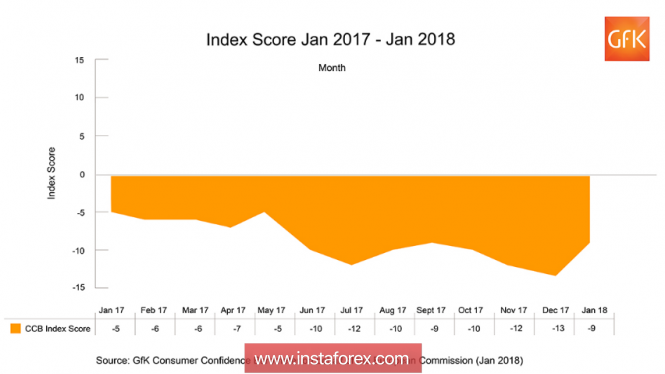

The consumer confidence index from Gfk unexpectedly rose in December from -13 to -9p, experts did not expect changes. The growth of the index reflects changes in the mood of the British, who expect improvement in their financial prospects in 2018. At the same time, the index is lower than a year ago (-5p), there is no good news about the increase in wages, and most likely, its positive impact will be short-lived.

The head of the Bank of England, Mark Carney, told in Davos that Brexit costs the UK economy 200 million pounds a week, after the announcement of the vote, the country has already lost 10 billion pounds of GDP. Speaking in Parliament, Carney noted that he sees signs of wage growth against the backdrop of growing demand for labor. Regarding inflation, Carney said that the fall of the pound in June 2016 will have an upward impact on inflation for several more years, but the positive effect of the fall of the currency has almost been completed.

Perhaps Carney with his speeches sought to reduce positive expectations and hinted that the reasons for yet another rate hike are still rather weak. He managed to do it badly. The pound still has a strong impetus for growth, which has not yet been worked out. Support is the recent low of 1.3977, but before the publication of the report on employment, trade in the lateral range is more likely.

Oil and ruble

After a slight correction, the March futures for Brent again approached the level of 69 dollars per barrel, the quotes are practically unaffected by the latest data from the USA, according to which the production volumes reached a maximum in 47 years, and the stocks of crude oil increased more than last week.

This week, the reporting of major oil companies will begin to be published, players will respond depending on how the dynamics of investments in the industry and profits change. So far, oil remains in the ascending channel, the probability of a return above $ 70 / bbl. regard as high.

The ruble is trading in a narrow range, demand for it remains stable, which is supported by good macroeconomic indicators and record demand for OFZ. Movement to 55 rubles / dollar looks priority.

The material has been provided by InstaForex Company - www.instaforex.com