Eurozone

According to the macroeconomic studies published last week, the expansion period of the eurozone economy that lasted for at least two years is coming to an end.

The evaluation of the ZEW Institute that showed a slowdown in growth rates was confirmed by other studies. All three PMI Markit indices came in worse in January than in December, despite the continuous expansion, the rates are slowing down.

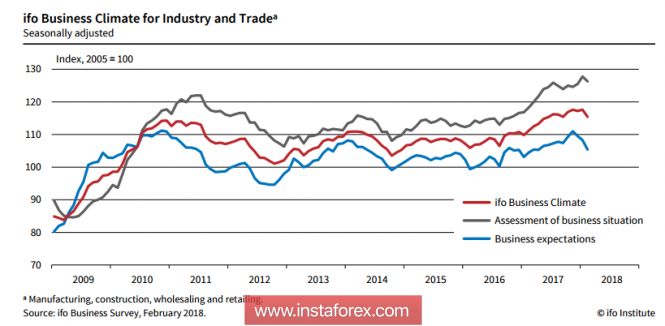

Business climate indices and economic expectations of IFO in February, significantly slowed down, while the expansion phase is completed. Companies are less satisfied with the current business situation, as euphoria is coming to an end, indices are falling across the entire spectrum of the economy specifically in production, wholesale, and construction.

The minutes of January meeting of the ECB was published on Thursday, which contained a number of disturbing statements. In particular, a number of ECB members expressed displeasure with the intention of the US authorities to help administrative measures to reduce the dollar, which, among other things, will be reflected in damage to the European economy and reduce import prices.

The ECB has no unity on the continuation of soft policy since strong economic performance and the growing euro prevents finding the balance.

On Wednesday, inflation data will be published in the euro area for February. While the outlook is negative which could possibly decline to 1.2%, and will help reduce the euro, update the February lows and attempt to reach the support zone at 1.2105 / 40.

United Kingdom

The British pound reacted by reducing the number of negative macroeconomic data. The GDP growth in 4 square meters is composed of 1.4% only, which is lower than expected. The weak data is because of the decline in the consumer demand amid high inflation, which is the minimum result for 5 years.

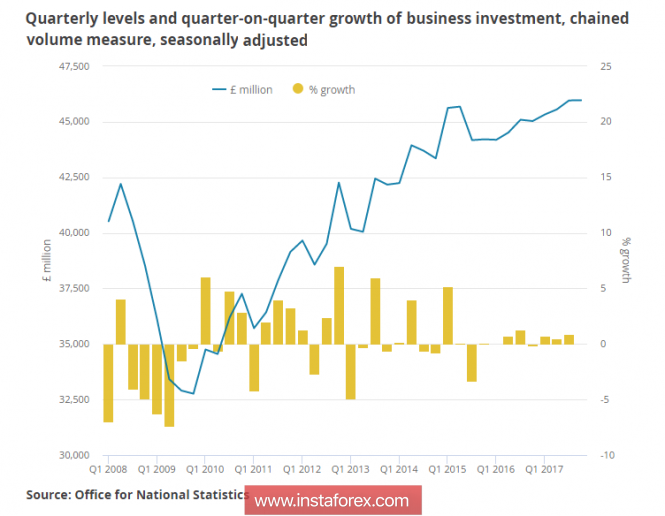

The increase of commercial investment in 2017 was 2.1% with a forecast of 2.4%, the growth was unexpected to be completely zero in the fourth quarter.

According to CBI, the growth of retail sales continues to slow down, the overall balance has decreased to + 8p against + 12p in January, which indicates a decrease in household incomes.

The pound is under pressure despite the favorable external background. Briefly, the dollar looks stronger but the positive expectations from the Brexit talks on March 22-23 will soon start to have a stronger impact. The formed wedge is threatened with a breakthrough, but its horizontal pattern does not provide an opportunity to indicate the direction. The Support can be found at 1.3855, and the resistance is at 1.4008.

Oil

Oil received a number of positive signals last week, which allowed the quotations to come back to the level of $ 70/ barrel. The first factor was the publication of the report from the US Department of Energy, which states that hydrocarbon reserves were reduced by 1.6 million barrels against a backdrop of sustained production growth. While the markets expect an increase in inventories of 1.9 million barrels.

OPEC was inspired by the success of collaboration intended to change the setup of relations into a long-term direction, for which experts from both OPEC and independent producers are working on. The structure of a new partnership will begin to operate after the expiration of the current agreement in late 2018.

Oil has the potential for further growth, which is supported by the sustained recovery of the world economy against the backdrop of controlling production volumes. If Brent quotes will be able to hold above 64.20 until next week, it is likely to establish a next high close to January's 70.82.* The presented market analysis is informative and does not constitute a guide to the transaction.

The material has been provided by InstaForex Company - www.instaforex.com