On February 5, the US stock indices collapsed at a record 4% over the past six years and the Dow Jones index fell 4.6%, which is the worst fall in a day in history. In the next morning, European exchanges have gained momentum followed by a drop in the Asian after the American indices.

Why did the exchanges fall? As it turned out, there is no rational answer. Yes, the Friday labor market report was significantly better than expected, which led to fears that the U.S. Federal Reserve will raise the interest rate more aggressively than anticipated and help cool the growth rate. However, these fears concerned only one possible additional increase in 2018 and could not serve as the reason for such large-scale sales.

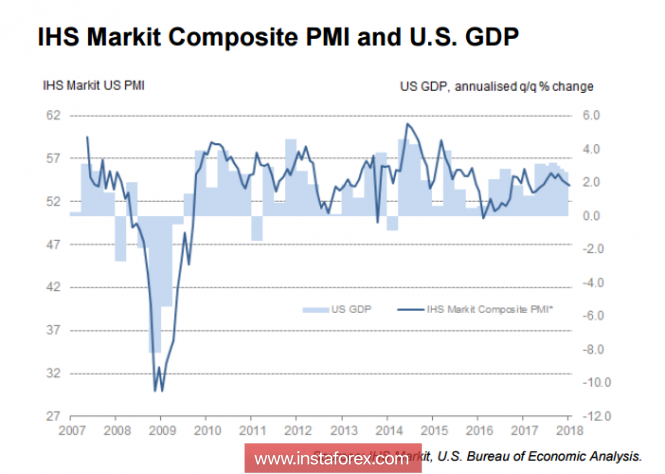

Macroeconomic indicators indicate a steady and stable growth. On Monday, the PMI Markit index for the services sector came out at 53.3p, which corresponded to the forecasts and values of December.

A similar index from ISM showed growth to 59.9p, significantly exceeding the forecast, which in the end should lead to an increase in the positive, and not to a decrease.

As for the rate forecasts according to the CME futures market data, they remained at the same level. The markets are waiting for an increase in March and June, and one more at the end of the year. The assumption that the markets were frightened of the fourth additional increase in the current year is not yet confirmed.

So what caused the fall of the markets? There is no rational explanation. The S&P 500 closed on Monday with the longest period of growth without correction in the last 20 years, which could mean an extremely powerful technical correction request. Hence, the stock market dropped on Friday after the publication of the employment report and trade robots entered the business, which signals fixing profits and sales.

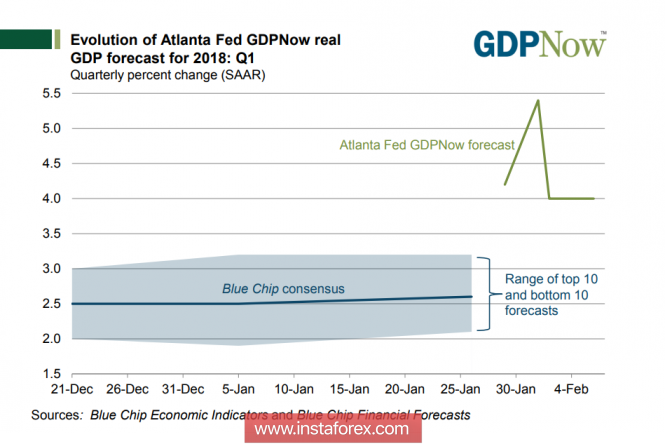

If this assumption is true, the stock markets should again begin a period even if there is no growth, then at least a recovery to the reached highs. There are simply no reasons for continuing sales. The February index of economic optimism from IBD / TIPP shows a steady growth to 56.7p against 55.1p, while the GDPNow model from the Atlanta Federal Reserve Bank predicts US GDP growth in the 1st quarter at 4%, which in no way indicates a slowdown.

The domestic political situation in the United States is also under control. Minister of Finance Mnuchin, anticipating the meeting of the Congress on the issue of the ceiling of the national debt, said that the fundamental indicators of the market are quite strong, and he is not concerned with "market volatility." In other words, it means not to pay attention to the fall of markets, raise the national debt, and everything will be in order.

Congress adopted the interim budget until February 23, so the shutdown was avoided. Temporary financing of the budget has been ensured. The tax reform comes into effect with the situation under control - that's how the situation looks like for the Wednesday morning.

Markets began to return in a calm state following various events including the slight decline of gold, rise in oil prices and stock indexes closed in the green zone which plays nearly a quarter from the recent fall. Sales are likely not to develop in creating a negative background. a new strong factor is needed and has to wait some more time given the good macroeconomic indicators.

The dollar reacted neutrally to sales, which underscores once again the lack of a link between the fundamental state of the economy and the collapse. Despite the fact of what Mnuchin said on Wednesday that he is committed to a strong dollar, the Ministry of Finance is likely to stick to its slow easing, which will help to balance the budget and somewhat narrow the gap between income and expenses.

Today, the situation in the U.S. economy will be commented on by several members of the FOMC, including Dudley. Most likely, they will try to calm the markets and confirm the policy of the unchanged policy of the Fed. Given the absence of important macroeconomic publications, the markets will trade in a tapering range by the end of the week. The dollar will weaken against European currencies, primarily against the franc and the euro, although a slight strengthening is possible against its commodity currencies.

The material has been provided by InstaForex Company - www.instaforex.com