The dollar finished the week with an absolute favorite, helped by the positive macroeconomic data released on Friday.

The index of expenditure on personal consumption in the first quarter of 2018 grew to 2.5% against +1.9% from the quarter earlier, which indicates a steady increase in consumer demand. The simultaneous increase in employment costs by 0.8% led players to the conclusion that the growth of consumer activity has a stable base, which will be supported by outstripping growth in household incomes. Both indicators exceeded forecasts and played a decisive role in strengthening the dollar.

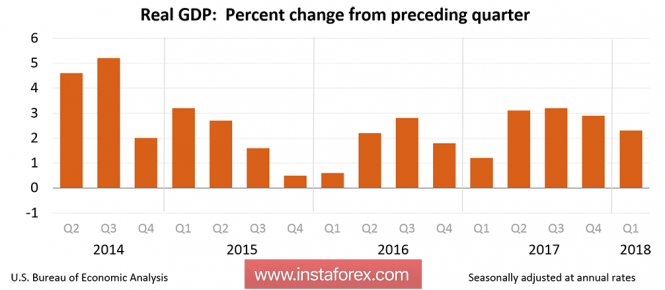

As for GDP growth, there was a surprise for the players - the growth rate even fell to 2.3% against 2.9% a quarter earlier, yet it was significantly higher than the forecasts.

In addition, data showed growth of the consumer confidence index from the University of Michigan to 98.8p in April, the steady growth in orders for durable goods, which supports industrial activity, and even unexpectedly strong reduction in the commodity balance deficit in March to come to a conclusion - demand for the dollar is maintained, in including, and the steady growth of the American economy, and not just the growth of geopolitical tensions.

The calendar for the next week is saturated, and the dollar may get a new impetus to growth on Monday, when the data on the price index of PCE, reflecting the dynamics of spending on personal consumption, will come out. Analysts expect growth in March to 1.8% against 1.6% in February, which will also contribute to the growth of core inflation - the main price criterion monitored by the Fed in the development of monetary policy.

On Tuesday, reports from Markit and ISM on activity in the manufacturing sector will be published, some slowdown in growth is expected, which, nevertheless, will remain confidently high.

On Wednesday, the next meeting of the FOMC will take place, which will not make any significant changes to the foreign exchange market, since it is "passing", that is, it is not accompanied by the publication of updated macroeconomic forecasts and a press conference. Attention of players will be riveted to the text of the accompanying statement, but it is unlikely to be very different from the previous one, the markets are waiting for another rate hike at the meeting in June, this step has already been fully appreciated and included in the quotations.

On Thursday, preliminary data for the 1st quarter on the labor market will be published, in particular on the growth rates of wages and productivity, as well as the ISM index for PMI in the services sector.

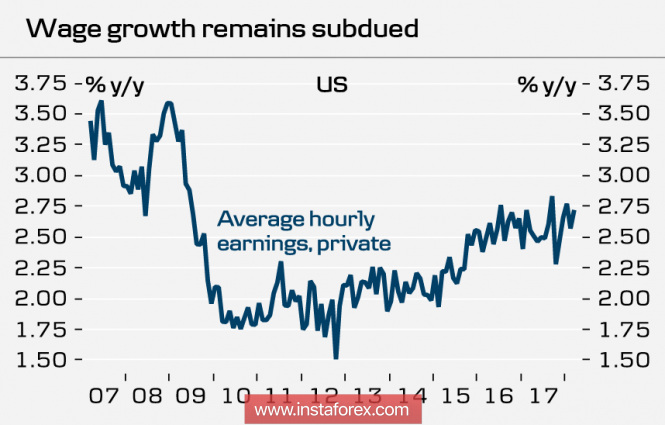

The key day of the week is Friday, when the employment report for April will be released. The number of new jobs may be closer to 200 thousand after weak data for March, but the main attention will again be riveted to the growth rates of wages. Markets need to understand why, with a steady growth in the labor market, inflation remains subdued, and if they see a positive response to their questions by the end of the day, the dollar will again close the week with a confident growth.

Strengthening of the dollar occurs against the backdrop of the indecisiveness of other central banks. On Thursday and Friday, the ECB and the Bank of Japan held regular meetings respectively, following which both currencies continued to surrender their positions. The ECB directly avoided any specific instructions on the timing of the completion of the repurchase program. The Bank of Japan left the rate on negative territory and confirmed its readiness to target the yield of 10-year bonds at the near-zero level, while the statements about plans to achieve a 2% inflation target disappeared from the accompanying statement, in 2019. We add that a week earlier, Mark Carney hinted that the Bank of England would not rush to normalize, and thus, the world's largest currencies politely gave way to the dollar, offering him the continuation it rallies.

A strong dollar is not needed by the US government, since it will complicate the fight against the budget deficit, but, apparently, this is inevitable at the current stage.

The material has been provided by InstaForex Company - www.instaforex.com