Last weekend in Mexico, presidential elections took place. The results of it can change not only the domestic scene but also the foreign policy of the country. Oddly enough, the Canadian dollar has become one of the beneficiaries of the current situation. The new president of Mexico, Lopez Obrador, can shift the NAFTA negotiation process away from a deadlock, especially since the American president is not in a hurry to leave the deal.

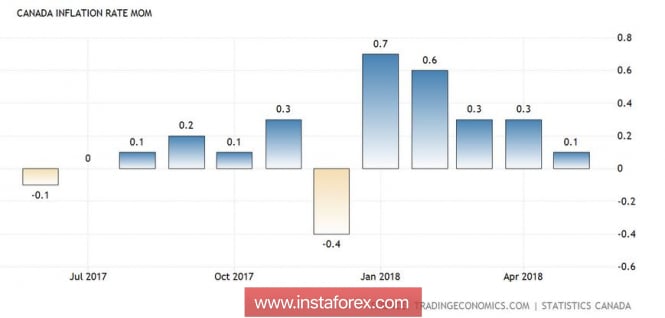

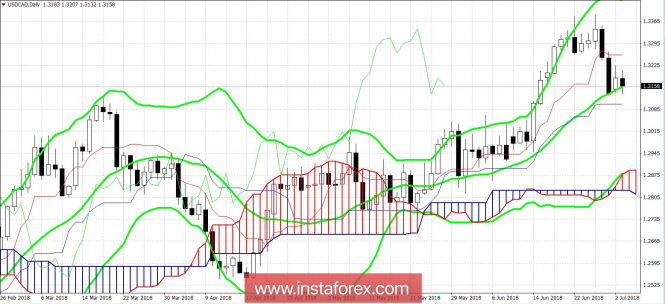

Having reached the annual peak of 1.3385, the USD / CAD pair began to creep down and literally within a few days, reached the middle of the 31st figure, where it is now being traded. The June weakness of the Canadian dollar is due to several reasons. First, the key macroeconomic indicators slowed down. The country's GDP grew by only 0.1% in April, while in March, this indicator reached 0.3%. Inflation also showed a weak growth with only 0.1% on a monthly basis, while in annual terms the indicator remained at the level of the previous month at 2.2%. The level of average hourly wages slightly decreased and the number of jobs in Canada declined by 7.5 thousand after a decrease of 1.1 thousand a month earlier. Analysts had expected the growth of this indicator at 23.5 thousand, so the published data disappointed the market.

Despite the slowdown in the dynamics of the growth of key indicators, the country's economy remains in good shape, especially in the context of further tightening of monetary policy conditions. After all, in annual terms, inflation remains above 2%, the unemployment rate is at a record low level of 5.8%, and the sharp decline in the number of employees is explained by weather factors. In addition, the production PMI in June reached a record high, updating the 8-year record.

Given this picture, we can conclude that the main risks for the Canadian dollar are not related to internal macroeconomic factors, but with external fundamental factors. First of all, we are talking about oil and the prospects for the North American Free Trade Agreement (NAFTA). And if oil traders survived the key event of the half-year, the OPEC + meeting, then the issue of trade relations between the US, Canada, and Mexico is still on the agenda.

The difficult negotiations have lasted for almost a year, since the US side voiced its conditions in the form of an ultimatum. With the arrival of the new Mexican president, there were hopes in the market that the situation would move from the deadlock. Lopez Obrador has already stated that he will maintain close and friendly relations with the States, including within the NAFTA.

Such prospects were inspired by the bears of the USD / CAD, although the Canadian side does not show such friendliness towards the White House. However, if, with respect to Mexico, Donald Trump can apply the "carrot method", then with regard to his northern neighbor, he can also use the "whip". It is important to note that the US president recently voiced the intention to introduce duties on all imported cars (previously it was only a car from the EU).

Such a move would be a tangible blow to the Canadian economy. Canada's auto industry mainly consists of car assembly plants of such auto giants including Toyota, Honda, Ford GM and others. At the same time, Canada exports to the US is more than 70% of cars produced in the country for about $ 50 billion. If Trump realizes his plans, the consequences can be very serious, right up to the recession of the economy.

According to some experts, Trump leads a policy of compulsion towards Canada. This week, negotiations will resume but they are unlikely to be completed in the coming months. Last weekend, the US president said that he would not take any decisions on the NAFTA until the midterm elections to the US Congress.

Here, the American president can be understood: on November 6, the Lower House of Congress (House of Representatives), as well as 35 senators out of a hundred, will be re-elected. In addition, the Americans will re-elect 39 state governors. The White House should assess the new political alignment in the Lower House before taking drastic decisions on the NAFTA.

In other words, the Canadian dollar received a temporary respite. First, Trump does not break the deal and waits for November; secondly, the trilateral talks will be resumed in the renewed composition; Thirdly, the new president of Mexico is less categorical towards the United States than his predecessor.

Such a fundamental picture allows us to say that the Bank of Canada will still raise the interest rate at one of the next meetings, especially given the positive dynamics of oil quotes. The combination of the above factors pulls the pair to the 30th figure, with the prospect of further decline to spring lows. The nearest price target for the southern movement is 1.3105 (the support level that corresponds to the Kijun-sen line at D1). Having overcome this target, the pair will be fixed in the 30th figure. Further prospects for the pair will depend on the determination of the Canadian regulator. If the Central Bank shows its intention to raise the rate in July, the USD / CAD will again return to the area of 20 figures.

The material has been provided by InstaForex Company - www.instaforex.com