The dollar strengthened its position by Friday, since much of the macroeconomic data published the day before was higher than expected.

GDP growth in the second quarter was confirmed at 4.2%, while the price index instead of the expected decline from 3.2% to 3.0% rose to 3.3%, also slightly higher than the forecast was the personal consumption expenditure index PCE Core, 2.1% vs. 2.0%. The latest data somewhat dissipate concerns about the slowdown in inflation and contributes to the growth in demand for the dollar.

Also, positive should be considered the growth of orders for durable goods by 4.5%, which significantly exceeded forecasts, although, in absolute terms, growth was significantly lower, because a strong decline was observed a year ago.

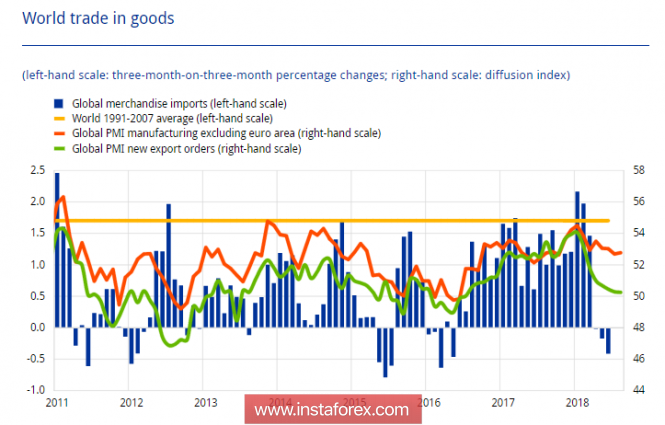

At the same time, the commodity balance has established another anti-record. In August, the deficit reached 75.83 billion dollars, which is noticeably worse than forecast. There is a steady trend of slowing trade in the world, the forecasts are gloomy, as the tariff war, which affects so far a small amount of goods, increases global uncertainty.

The yield of 10-year Treasuries so far remains at just above 3% and does not show a desire for growth, which somewhat limits the growth of the dollar. However, if long-term expectations for the rate begin to grow, for which the prerequisites are now taking shape, profitability will also go up, which will mean a decrease in demand for bonds and an increase in demand for a cash dollar.

The most significant factor that can prevent the dollar from starting its triumphal growth is the objective aspiration of Russia, China, and Europe to create a system of settlements that exclude the dollar. It is to this scenario that the entire US policy objectively pushes the world, and the first step in this direction could be the creation of a circumvention system for the US ban on trade with Iran, as the EU has already directly stated.

Eurozone

The euro fell on Thursday, responding to rising dollar expectations, as its own benchmarks in the eurozone are fairly stable and do not indicate the possibility of a strong decline in the short term.

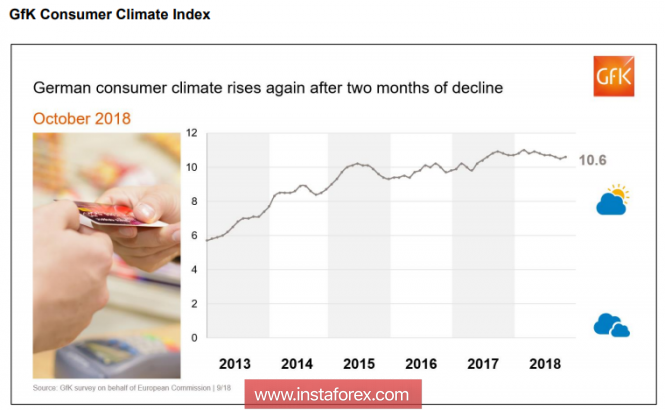

The consumer confidence index from GfK rose in September to 10.6p against 10.5p a month earlier, optimism in the field of economy and personal incomes is obvious, despite political instability. The index corresponds to a similar study from IFO, published on Monday.

Also, quite positive are the data on inflation in Germany, previously in September, the growth was 2.3%, this is higher than the forecast of 2.0% and gives grounds to expect that Eurostat's current report on inflation in the eurozone will be at least as good as expectations, which in the end can support the euro.

The currency pair EUR / USD remains under pressure on Friday, the probability of a decline to support 1.1590 is quite high. In the case of negative data, the movement to 1.1526 is possible.

The United Kingdom

The situation with consumer confidence in the UK is completely different, the GfK index fell to -9p in September, losing two more points in a month. Expectations for personal financial well-being are still in the positive zone, this is the last criterion that does not let inflation expectations collapse, but as for the economy as a whole, the situation here is completely different. Brexit is only six months away, the absence of a deal will lead to a drastic reduction in consumer confidence, which will inevitably lead to a decrease in consumer demand and a slowdown in the economy.

Today, updated data on GDP growth in the 2nd quarter will be published, as well as on the dynamics of investment and the balance of payments. Neutral forecasts, if there is no deterioration, the pound will get some support.

The currency pair GBP / USD can test the support for 1.3053 for strength, growth attempts will be used for new sales, the forecast for Friday is negative.

The material has been provided by InstaForex Company - www.instaforex.com