The turmoil with Brexit overshadowed the dynamics of the US currency, which, by chance, continues to increase its positions on the sly. The dollar index continues to be around one and a half year highs, reflecting the steady demand for the greenback. However, not all pairs are dominated by the dollar – for example, in the pair with the yen and the New Zealand dollar, the situation is mirrored, and the GBP/USD pair is completely at the mercy of Brexit, completely ignoring American events.

But in general, the greenback did not fall off its peak after the elections to Congress, as predicted by many experts. As a result of the elections, the most predictable result was realized (although very unpleasant for the dollar), therefore the weakening of the national currency was temporary. This was followed by quite positive signals that returned confidence to dollar bulls. First, the head of the White House extended a hand of friendship to the Democrats, offering cooperation in terms of the legislative process. And although this curtsey will not save him from a wave of new investigations, nonetheless Trump was able to neutralize nervousness about the possible imbalance of the American political system. Secondly, the US has recently pleased dollar bulls with strong macroeconomic reports. In particular, the labor market traditionally supported the greenback.

Thus, unemployment remained at a record low of 3.7% (the lowest since December 1969), and the unemployment rate of U-6 (that is, taking into account part-time employees) fell to 7.4% last month (in September it was at 7.5%). The number of employed in the non-agricultural sector increased by 250,000 people in October, and the share of the economically active population in the United States rose to 62.9%, showing a positive trend. What is especially important – the growth of salaries accelerated in October. This indicator is closely monitored by the members of the US central bank as its growth or decline demonstrates the level of demand in the labor market and indirectly affects the dynamics of inflationary pressure. According to most economists, for inflation to move to its target level, wage growth in annual terms should be above three percent.

So, in October, this indicator exceeded the key target and amounted to 3.1%, confirming the forecasts of experts. But in order for the puzzle of inflation growth to be fully formed, it was necessary to neutralize the September slowdown in the consumer price index. Then the numbers were frankly disappointing, causing some anxiety in the ranks of dollar bulls. However, the data published this week reassured investors, despite the fact that the release did not exceed the forecast values.

However, experts expected the growth of the CPI, and their expectations were fully justified: on a monthly basis, it reached three-tenths of a percent, and in annual terms, the indicator also came out at the level of forecasts, being at the level of 2.5%. Excluding food and electricity prices, the indicator similarly showed the dynamics of growth. On a monthly basis, it rose to two-tenths of a percent, and on an annual basis to 2.1 percent. However, the core inflation did not reach the forecast level, but it is not critical against the background of the general dynamics.

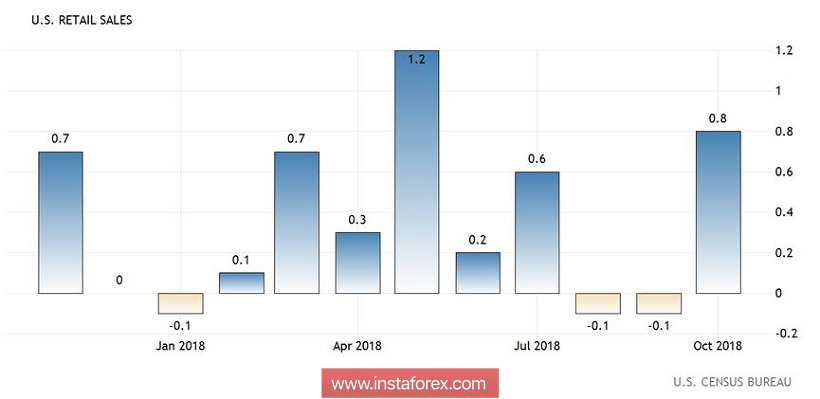

If we talk about the dynamics of US economic growth, we can not fail to say about today's release. Retail sales also showed a significant breakthrough after a rather weak dynamics in August and September. But in October, the figure came out better than forecasts - both with and without car sales. Consumer activity of Americans also plays an important role for the Fed, as the indicator reflects the growth rate of the country's economy.

All this allows Fed Chairman Jerome Powell to keep the course for further tightening of monetary policy. During the last 24 hours, he gave a speech twice at various events in the United States, answering questions from the audience. After the first speech, the dollar index fell slightly, because Powell, according to the market, took a rather cautious position regarding future prospects. But during the second speech, he "rehabilitated" - in particular, he said that market participants should get used to the idea that the Federal Reserve will gradually but steadily increase the base interest rate. In addition, he recalled that next year he will hold press conferences on the results of each of the eight meetings of the Fed, hinting that the rate can be raised at any of them (now the decisions of the regulator are expected only at extended meetings).

Summarizing the above, we can conclude that the general fundamental background allows the Federal Reserve to further tighten monetary policy: the probability of a rate hike at the December meeting is estimated at 70%, at the first spring meeting next year – at 45%. Recent macroeconomic reports and comments of the Fed's heads once again convinced the market of the regulator's "hawkish" intentions.

The material has been provided by InstaForex Company - www.instaforex.com