The dynamics of producer prices in May was close to forecasts, the growth was only 0.1%, business optimism indices from NFIB and IBD/TIPP gave the opposite results, without adding clarity.

Markets traded neutrally, taking advantage of the temporary respite due to the lack of news from the fields of the trade war between the US and China, but the surge of a new wave of panic in the coming days is becoming more likely. China, focusing on changing the rhetoric of the Fed, has already announced new tax incentives aimed at financing infrastructure projects, that is, exactly what Washington is trying to limit.

The pause may last until the G20 meeting on June 28-29, but the lack of positive news in itself can return panic and provoke a new wave of demand for protective tools.

EURUSD

The indicator of investor confidence Sentix fell in June to -3.3 p, falling by 8 points. In Germany, the situation is even more serious, as the overall index for the first time since March 2010 returned to the negative territory, which makes the recession very likely.

Moreover, despite the confidence of the US President that he is winning the trade war, this Pyrrhic victory does not support the US economy. The overall US index fell by more than 10 points to its lowest level in February 2016.

The ECB, as expected, changed its rhetoric, extending the period of unchanged interest rate to at least the middle of 2020, so the markets do not expect any changes in connection with the transition of the ECB to the easing regime. If the economic situation continues to deteriorate, which in turn will call into question plans to achieve the target level of core inflation, the expansion of incentives will become inevitable. Already, market inflation expectations are close to historical lows.

Today, comments on monetary policy will be addressed to different audiences by Draghi, de Guindos and Coeure, and their task is to try to prevent the euro growth against the background of changing expectations on the rate of the Fed, so the markets can hear something new on the details of the implementation of the incentive program TLTRO3.

On Wednesday morning, the euro is trading in the range near 3-month highs, expected growth to 1.1375/85 and further to 1.1448 did not take place due to a very weak Sentix index and the bank holiday, trading in the range with a high probability will continue today. An attempt to update the recent high of 1.1347 is expected, but there is little chance of steady growth.

GBPUSD

Unemployment in the UK remained at 3.8% in February – April, which is in line with forecasts, the average wage increased by 3.4%, and taking into account premiums – by 3.1%. The pound reacted with a slight increase, but the upward movement is unlikely to develop, as in favor of reducing the grounds much more.

On Monday, we predicted the growth of GBPUSD to 1.2762/72 and further to 1.2863, the first goal was achieved, but then the upward movement of the pound was stopped by an extremely weak report on industrial production. The decrease in April was 2.7%, in the manufacturing industry -3.9%, year-on-year indicators also went negative to -1.0% and -0.8%, respectively. Moreover, NIESR lowered its quarterly GDP growth estimate from 0.4% to 0.1%, with markets expecting growth of 0.5%, and such a low estimate means that the UK has only one step left in the recession.

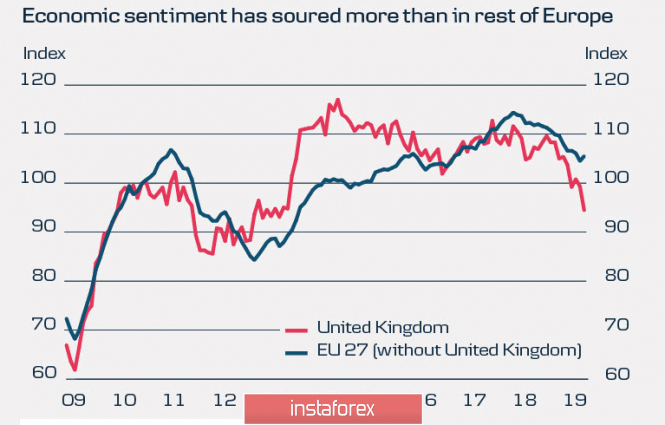

In such conditions, it is not necessary to count on the growth of investments. Economic sentiment in the UK business environment remains depressed and looks much worse than in the rest of Europe. The decline in sentiment is largely due to a decline in business confidence and political uncertainty.

Both Labor and Conservatives are losing the trust of voters, yielding to the fast-moving pressure of Nigel Farage's new Brexit party, urgent elections will be a disaster for conservatives who will lose many seats, and three years after the referendum, there is still no clarity on the scenario of the UK's exit from the EU.

The pound goes into the side range, the boundaries of which 1.2653 – 1.2762 will restrain volatility, macroeconomic news is not expected until the end of the week.

The material has been provided by InstaForex Company - www.instaforex.com