Today, just when there is literally a few hours left before the announcement of the decision of the Federal Open Market Committee of the United States, the title issue is fundamental to understanding what will happen in the markets in the next three months. While one thing is clear - at the current meeting, the key rate will not be lowered. However, the farther into the forest, the thicker the partisans, but still try to sort out this issue.

The Fed's actions are regulated by the Federal Reserve Act, where two goals are set as the main objectives: controlling inflation and maintaining employment at high levels. According to this law, inflation targets should be 2% in the medium term, and the unemployment rate should be below 4.5%, although this is an unofficial indicator.

Among other factors affecting monetary policy, the US Federal Reserve Committee on Open Market (FOMC) monitors the situation in the stock market, which is the basis of the well-being of the middle class. Also taken into account are other indicators of the economy and monetary circulation, which, although they are important elements of the assessment of the economic situation, still only complement the main objectives.

The Committee (FOMC) holds eight meetings per year, of which four meetings are held at the end of each quarter - in March, June, September and December - we call them "main". Four other meetings - in January, April, July and October - fall in the middle of the quarter, we call these meetings "additional". Previously, the "additional" meetings, in contrast to the "main" meetings, were one-day meetings. Later on, these meetings became two days, but were held without a press conference. In 2019, the Fed changed the order of the "additional" meetings, and now after them, as after the "main" meetings, a press conference of the Fed chairman is held, in this case, by Jerome Powell.

From 2019, the main difference between the "main" meetings and the "additional" is the publication and voicing of the FOMC forecasts and its view on the economic situation: an employment and inflation forecast is published, GDP growth prospects are given, the views of the future monetary policy committee members "Dot charts".

To determine the objectives of the Fed's policy, traders use the FedWatchTool tool from the CME futures exchange, which assesses the likelihood of a rate increase as traders who trade in futures on federal funds see it. According to the indicators of this instrument, traders do not expect a rate increase at the June meeting, 79.2% of them believe that the rate will remain in the current band of 2.25-2.50 percent. But then miracles begin, and 66.5% of traders believe that the rate will be trimmed by 0.25% at the meeting on July 31, another 17.5% believe that the rate will be reduced by 0.5%. Thus, 84% of traders predict a rate reduction at the next meeting!

To be honest, I don't really understand this opinion about the current situation, so let's deal with the causes and consequences of this situation.

Now, Donald Trump has unprecedented pressure on the Fed, which for some reason does not cause outrage in the United States. Other actions of the US president may infuriate the American press, but not his criticism of Fed Chairman Jerome Powell and interference with the work of the central bank. So, answering the question whether he wants to dismiss the head of the Fed, Trump told reporters on Tuesday: "We'll see what he does!".

Earlier, the Trump administration was considering the possibility of Powell's removal from his post, but now, according to the White House's economic adviser Larry Cudlow, the administration is not considering this step. Trump's wishes are, of course, a serious thing, but, unfortunately, for the US president they are not spelled out in the Federal Reserve Act. The law spelled inflation rates and high employment. Let's see what happens with these key indicators.

Here is what CNBC writes about this: "Now that the labor market is showing signs of tension, economists and investors firmly believe that the Federal Reserve will begin lowering rates by next month. The economy added only 75,000 jobs in May, which is 100,000 fewer than expected, a sign that the slowdown that is emerging in other parts of the economy currently affects the labor market." The following are the words of the chief economist of the Wilmington Trust: "I think this is a real slowdown in hiring. Sometimes you can neglect monthly volatility a bit, but I think we have enough signs. "

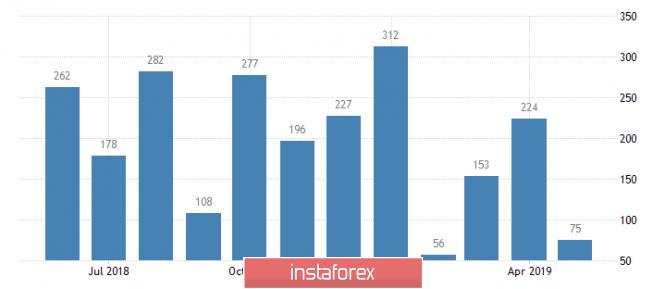

Figure 1: Newly created jobs in the United States.

Oh, horror, horror, horror! But still look at the data on the newly created jobs. Indeed, only 75 thousand jobs were created in May, but 224 thousand were created in April, 153 thousand in March, 56 thousand in February and 312 thousand in January. The year 2017 created 200 thousand jobs per month, then 175 thousand were created in 2019. However, employment also increased! At the beginning of 2016, unemployment was 5.2%, now its level is 3.6% (Figure 2), and this is already an overheating of the economy. Here it is time to raise the rate, and not to lower it!

Fig.2: Unemployment in the USA

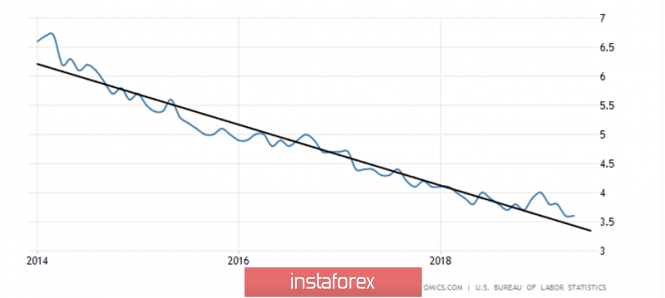

Now look at inflation. The core inflation indicator, i.e. excluding food and energy, the Fed uses it to analyze the situation, is now 2% (Fig. 3). The consumer inflation rate is 1.8%, and consumer inflation is now growing, and it has grown from the level of 1.6% since the beginning of the year. This should take into account the fact that consumer inflation has not yet been affected by Donald Trump's actions, who increased duties on Chinese goods. Indeed, there are some rates of slowing inflation, but certainly they are not so terrible that the Fed will take emergency measures.

Figure 3: Core inflation

Perhaps slowed US GDP growth? Again, no, GDP is growing at a rate of 3.2% per year, and so far no signs of a slowdown have been found. Then maybe the stock market is declining, which is causing concern for the middle class and Wall Street gatekeepers? Again, no! The Dow is just a couple of hundred points away from record highs.

The Fed's greatest concern is the inversion of the yield curve in the bond market, when the yield of government treasury bonds with a short maturity becomes higher than the yield of bonds with a longer maturity. Yield inversion is considered a "true" sign of a near recession in the economy, but is this enough for emergency measures? Is it necessary to reduce the rate in July?

I think that the Fed can really go for a two-fold rate cut in September and December, but on the whole it is unlikely that it will do it in July. However, here I can be mistaken, the future actions of the Fed are too unequivocally interpreted now. Therefore, it is quite possible that the FOMC will indeed succumb to blackmail from the motley public, which today, like a financial addict, requires money for another dose.

In principle, there is no big difference for the Fed, to lower the rate in July or lower it in September. I can assume that in order to avoid problems and quietly go on vacation in August, the Open Market Committee will take such an unconventional step. However, then the Committee should be prepared for the fact that the Fed will demand money at every opportunity, because, according to the markets, the trees should and will grow to the skies!

The material has been provided by InstaForex Company - www.instaforex.com