The growth of uncertainty intensifies at the opening of the week on Monday. The Central Bank of China weakened the yuan against the dollar again. The rate has peaked since February 2008 while Asia-Pacific exchanges are trading in different directions.

The question of whether there will be a recession or not is no longer on the agenda. Now the American establishment has a completely different question, who will ultimately succeed in blaming it. Trump constantly claims that the Fed does not help the economy by maintaining too high interest rates and Jerome Powell even called the enemy of the state. In turn, the Fed is trying to avoid accusations of excessive politicization but Fed officials are inclined to consider Trump to be the main culprit in the onset of the recession, which, in their opinion, with clumsy actions in trade policy just destroys the basis for sustainable economic growth.

Former Fed official William Dudley said this week that "Fed officials can explicitly say that the Central Bank will not save the administration, which continues to make the wrong choice regarding trade policy, and it is clear that Trump will be responsible for the consequences of his actions."

These are signs of the start of a new presidential race. The parties indicate their positions and the US political and financial establishment is actively polarizing into two opposite camps. The Consumer Confidence Index showed the most significant monthly decline since December 2012, and the University of Michigan seems to be taking a side at the Fed in a heated debate about who is to be considered guilty of approaching the recession. The accompanying statement emphasizes that every third consumer who was surveyed mentioned tariffs as a negative factor. Such a policy may provide certain advantages in trade negotiations with China, but at the same time, it contributes to the growth of uncertainty and lower household consumption spending. It is noted that "undermining confidence is in full swing."

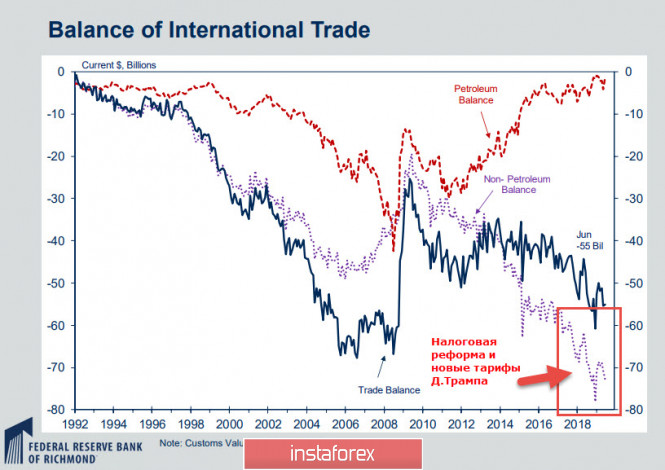

Other indicators look similar. Tips bond yields fell to the level of September 2016, that is, the business no longer sees the possibility of growth in consumer spending even against the backdrop of the tax reform. ISM notes a sharp slowdown in business growth and the trade balance, excluding petroleum products is showing a record drop.

According to the CME futures market, the probability of two rate cuts is consistently high this year. This means that the Fed will lower the rate and will be forced to announce a slowdown in economic growth. With a high probability, the Fed meeting will be a turning point in the recognition that the global economy has turned to a new crisis.

The recognition of this fact will consolidate the diversion of safe and protective assets in favor of the fall of the former and the growth of the latter. This is how the main trend for the coming month looks like. The dollar is definitely a defensive asset as the euro and the pound are likely to continue its decline.

EUR / USD pair

Core inflation in the eurozone remained at the same level in August, which turned out to be worse than forecasts suggesting a slight increase. The confidence of the markets that the ECB is preparing for the widest stimulus package at the next meeting is growing and this confidence is putting strong pressure on the euro.

The support of 1.1027 did not resist and the chances of returning above 1.10 look weak. It is more logical to use any growth for sales with the target of 1.0920/30. A decline to 1.06 is not ruled out for a long time.

GBP/USD pair

The markets have come to understand that, nevertheless, Britain will leave the EU by November 1 but some optimism is based on the fact that the exit will be orderly. In any case, attempts to increase the pound last week are interpreted that way.

As for economic data, there is no reason for optimism. Gfk's consumer confidence index updated the low again, dropping to -14p, which turned out to be worse than expected. PMI forecasts suggest a further slowdown in the economy.

The political struggle for the exit scenario from the EU is in full swing and the pound has nothing to rely on again. So, it is likely to resume the decline. Possible growth is limited by the zone to 1.2190/2202 with the nearest target of 1.2062, after its breakthrough the decline may increase.

The material has been provided by InstaForex Company - www.instaforex.com