Key central banks will hold their meetings on Thursday, October 24, and Wednesday, 29 and 30, which will determine the dynamics of financial markets for at least the next one and a half to two months, and maybe in the longer term. Given these important events, from the point of view of trading in the foreign exchange market, we need to make assumptions cleared of information noise, and then look at how our assumptions worked out in reality. In other words, we need to create an algorithm of actions and make changes to it in accordance with newly emerging circumstances.

However, why did I need to mark up a roadmap before and not after the event has already happened? There are a number of reasons for this, and first of all, my deep conviction that in the current situation, meetings of central banks will only confirm decisions already made earlier. Surprises are possible only from the Fed, but this seems unlikely. Therefore, while there are still some doubts regarding the actions of the Open Market Committee, I personally have no doubts about the actions of the European Central Bank.

First of all, traders should know that, according to the regulations, the ECB never comments on or regulates the euro or, at least, declares it in words. However, one must be very naive to assume the detachment of the regulator in the fate of the exchange rate of the currency accountable to him. In words, the Fed and the ECB pursue an independent monetary policy, but the ability to create surplus value from the issue of money helps maintain the high standards of life for the "golden billion".

Therefore, it's impossible for me to imagine that the change in exchange rates has been let off by gravity of key central banks. Well, if Russia holds consultations with OPEC countries to limit oil production and thus regulates the price, then the countries that are members of the North Atlantic alliance have been doing this for a long time and quite successfully, but with regard to money. Having in its hands a tool that controls 90 percent of the world's money circulation, it is a sin not to use this tool.

So, what do we currently know about the policy of central banks? The European Central Bank maintains a refinancing rate of 0% and re-launched a large-scale asset purchase program worth €20 billion per month, and did so simultaneously with new long-term refinancing programs, which should not only increase the availability of liquidity in the European market, but also stimulate the development of the European economics. According to many experts, this should serve to weaken the euro, but did it?

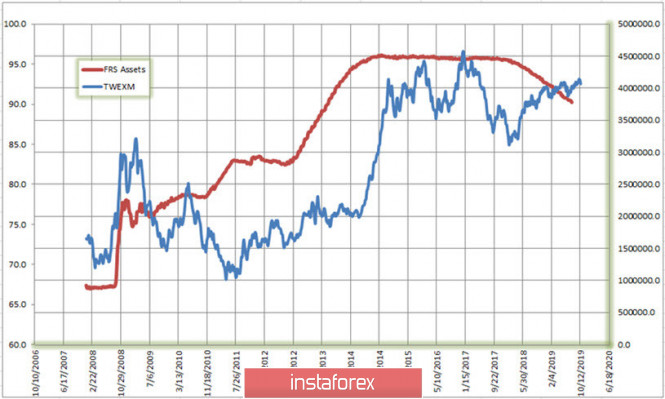

Having been hit by a liquidity crisis in the repurchase market that erupted in September, the Fed, under the formal pretext of increasing reserves of commercial banks, was forced to adopt an urgent program for the purchase of short-term bills of the US government totaling $65 billion per month. This at least equalizes the chances of the dollar in the competition of printing presses, if it does not increase its advantage. However, the truth is that the quantitative easing policy does not affect the exchange rate, at least to the extent that we would like to. You can see the evidence on the chart (Fig. 1), which shows the dynamics of the trade-weighted US dollar index calculated by the Fed based on the results of trade with leading world currencies.

Figure 1: Relationship between US Fed assets and the trade-weighted dollar index. Source - Federal Reserve Bank of St. Louis

Indeed, there are periods on the chart when the dollar depreciated with an increase in the Fed balance, but there are periods when everything happened exactly the opposite. A similar picture can be obtained by comparing the euro and the change in the balance sheet of the European Central Bank. The connection between the exchange rate and the balance sheet of the central bank may exist, but it is certainly not so primitive that we could calculate it using simple methods.

When assessing the prospects for exchange rates, one should rather be guided by dynamic changes in the interest rate differential in the EURUSD rate, an assessment of the yield of treasury instruments with the same maturity, inflation potential, growth prospects for prices of major commodity assets, positioning of leading traders in the futures market, and seasonal factors. You and I can try to evaluate something, but most of the factors will remain unknown to us. At the same time, trading in exchange rates is doing so in probability, and the more facts we can evaluate, the higher the probability of success for the transactions we make. The main thing in these factors then is not to get confused.

If we talk about the dynamic prospects of rates, then the advantage here is on the side of the euro. The ECB is in no hurry to make a refinancing rate below zero, and Mario Draghi, as a downed pilot, is rather concerned about how he can eject a golden parachute. He did everything he could, which at least presupposes a period of some stability in the policy of the regulator.

In turn, since July of this year, the US Federal Reserve lowered the federal funds rate by half a percent, from 2.25 to 1.75, meaning the lower limit of the range established by the Open Markets Committee. Today, 94% of traders believe that the Fed will go for another rate cut in 6 days, dropping it to the level of 1.50-1.75 percent. A decrease in differential by 0.75% over three months is a serious decrease in the possibility of earning by arbitrage operations. Therefore, it is not surprising that from the beginning of August, that is, from the moment the Fed rate was lowered, institutional investors gradually refused to place investments in US dollars.

During this time, the long positions of institutional management funds (Asset Manager) lost about a tenth, while euro sales by this category of traders in the futures market, on the contrary, increased. At the same time, asset managers have been the main buyers of the euro in the futures market since 2016, which was due to their hedging a short position in the cash market that accompanies transactions in investments in higher-yield dollar instruments.

Actually, the question now is not whether there will be a reversal of the downward trend in euros, but when it will happen. Last week ended with serious technical signs of breaking the fundamental trend on the EURUSD course. However, the reversal is not yet over, and its formation may last another one or two months, which is fraught for us with problems associated with the formation of a new direction, and the meetings of central banks that we will see in the near future may accelerate or may slow down the formation of the reversal. However, the probability of a EURUSD rate reversal is becoming more and more every day, take this into account when opening your positions.

The material has been provided by InstaForex Company - www.instaforex.com