The U.S. Federal Reserve is not going to abandon plans to normalize monetary policy. At least Omicron wouldn't make them do it. Fed Chairman Jerome Powell's speech to the U.S. Congress was more than indicative. The Federal Reserve intends to make every effort to curb inflation, considers the economy to be strong, and QE outdated. They are determined to wind down the quantitative easing program earlier than currently assumed. And this is extremely unpleasant news for gold.

Is it worth taking away the punch bowl just as the party gets going? This is the basic question that most central banks have asked themselves, looking at inflation soaring by leaps and bounds. Nobody wanted to return to the 1990s, but they had to. The acceleration of consumer prices to three-decade highs in both the U.S. and Europe is pushing central banks to fulfill their primary mission of regulating inflation. And if the ECB continues to adhere to the mantra about the temporary nature of a high CPI, then the Fed has abandoned it.

The appearance of the Omicron variant became a ray of light in the dark kingdom for the XAUUSD bulls. Rumors began to circulate in the market that the Fed and other central banks would put the brakes on normalizing monetary policy, which led to a drop in Treasury yields and a weakening of the U.S. dollar. Alas, the rise of the precious metal above $1,815 per ounce turned out to be his Swan Song.

The Fed is serious about speeding up the process of getting rid of QE, it could raise rates even before the US economy reaches full employment, and predicts that prices will remain at elevated levels in the first half of 2022. All of this paves the way up for U.S. bond yields. The rise in debt market rates was a sober reaction to Jerome Powell's speech to Congress.

Reaction of U.S. bond yields to Powell's speech

And although the gold bulls do not leave hopes for revenge, XAUUSD buyers are again faced with headwinds. According to Credit Suisse, the precious metal will cost $1,850 per ounce in 2022 since the Fed will only raise rates once, and inflation will continue to be at elevated levels, which will keep real bond yields at a historic bottom. There are hopes that the increase in borrowing costs will increase the risks of stagflation, which is good news for gold.

In fact, the U.S. economy is so strong that even a 100bp hike in the federal funds rate is unlikely to slow it down significantly. Powell and his colleagues are well aware of this and are determined to accelerate the cycle of monetary policy normalization. Moreover, the pressure on the precious metal in the short term may be exerted by the correction of U.S. stock indices. Monetary restriction and resuscitation of the public debt ceiling problem are strong reasons for the S&P 500 pullback, worsening global risk appetite, and flight to safe-haven currencies, including the U.S. dollar.

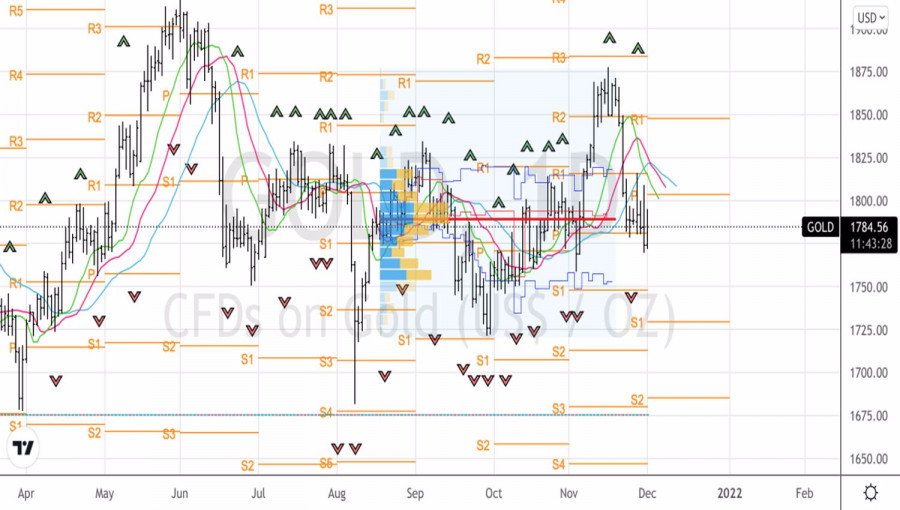

Technically, the inability of the bulls to return quotes above fair value by $1,790 per ounce is a sign of their weakness and a reason for selling in the direction of $1,750 and $1,720.

Gold, Daily chart